A debt management plan preserves your credit score; bankruptcy destroys it for 7–10 years. Debt Management Plan vs Bankruptcy Compare costs, timelines, what debts qualify, and the long-term financial impact of each option for 2026.

Debt Management Plan vs Bankruptcy in 2026: Which Option Saves More & Damages Credit Less?

Short answer (2026 view)

- A Debt Management Plan (DMP) usually damages your credit less than bankruptcy. It’s not a public record, doesn’t stay on your file as long as bankruptcy, and you pay what you owe (often at lower interest) instead of having debts discharged. A completed DMP can even help your credit rebound.

- Bankruptcy (Chapter 7 or Chapter 13) can save you more money in the short- to medium-term if you’re deeply over your head, because you may only repay a portion of what you owe—or nothing at all in a Chapter 7 liquidation. In exchange, it’s a severe, long-term negative mark on your credit report (10 years for Chapter 7, 7 years for Chapter 13 in the U.S.), and it’s a public court filing.

Debt Management Plan vs Bankruptcy; The “better” choice depends on your numbers: how much you owe, your income, whether you can realistically pay it all in 3–5 years, and whether you need the legal protection bankruptcy provides.

Below is a practical 2026 comparison plus a simple decision flow.

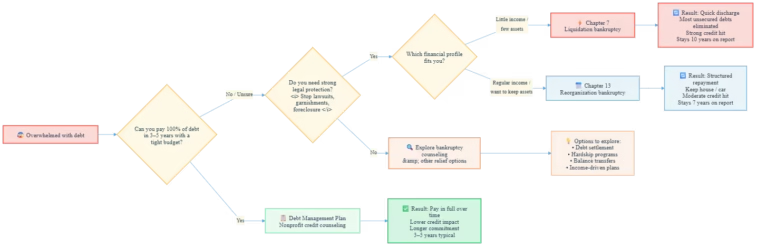

High‑level decision flow

1. What each option actually is (2026 basics)

Debt Management Plan (DMP)

- What it is: A structured repayment plan typically offered by nonprofit credit counseling agencies. You make one monthly payment to the agency; they pay your creditors. The agency negotiates lower interest rates and often gets creditors to waive certain fees. You pay the balances in full over 3–5 years.

- What debts it covers: Mostly unsecured debts (credit cards, some personal loans, utility-type bills). It usually cannot include: student loans, secured debts (mortgages, auto loans), tax debts, or certain other obligations. Loans generally can’t be included.

- Legal status: It’s a private arrangement/contract. There is no court order and no automatic “stay” that stops lawsuits or garnishments (creditors may agree to halt collection, but that’s voluntary).

Bankruptcy (consumer, mainly U.S.)

- What it is: A federal legal process that can discharge (forgive) some or all of your debts. For individuals, the two main types are:

- Chapter 7: “Liquidation” — many unsecured debts are wiped out; nonexempt assets may be sold to pay creditors. To qualify, you must pass a “means test.” Process is relatively quick (months).

- Chapter 13: “Repayment” — you pay into a 3–5 year court‑approved plan based on your disposable income; remaining qualifying debt is discharged at the end.

- Legal status: Once you file, an automatic stay stops most collection actions, including lawsuits and wage garnishments, and forces all eligible creditors into the case.

Note: Some of the detailed pros/cons below draw on U.S. sources; laws and exact credit‑report timeframes differ in Canada/UK, but the tradeoffs (pay‑in‑full with DMP vs discharge with bankruptcy) are similar in concept.

2. Debt Management Plan vs Bankruptcy; Direct comparison: Which “saves more”?

What “saving more” really means here

- DMP: You still pay 100% of principal (everything you borrowed), but you may save a lot on interest and late fees because the counselor negotiates rate reductions and fee waivers.

- Bankruptcy: You may pay only a fraction of what you owe (Chapter 7), or a partial amount over 3–5 years (Chapter 13) before remaining qualifying debts are discharged. In that sense, bankruptcy can erase more total debt than a DMP.

Total cost to you (out of pocket)

- DMP costs:

- Setup: Often around $25–$75; some agencies average ~$35 to set up.

- Monthly fee: Usually a modest flat fee or a small percentage of your monthly payment; one large nonprofit cites roughly $24/month on average. Over 4 years, that’s on the order of $1,000–$1,500 in DMP fees.

- You repay all principal (plus some reduced interest).

- Bankruptcy costs:

- Filing fees, mandatory credit counseling/debtor education courses, and attorney fees. Money Management International notes the process “can cost upwards of $4,000,” especially if you use an attorney (which is strongly recommended).

- In Chapter 13, you also make monthly plan payments to the trustee for 3–5 years—but those payments are often lower than your pre‑bankruptcy debt burden and based on what you can afford.

- In Chapter 7, many unsecured debts are discharged with little or no repayment (other than through asset liquidation), so you may pay far less than total owed.

So, which saves more?

- If you can realistically pay 100% of your debt within 3–5 years, a DMP typically saves you interest and fees while avoiding the heavy, long‑term credit hit of bankruptcy. You don’t “save” on principal, but you keep the obligation and pay less total over time than just keeping your high‑interest cards.

- If you cannot realistically pay everything off in 3–5 years (even with lower interest), or your debt is so large relative to your income that you’re trapped making minimums, bankruptcy often “saves” more in dollars because it discharges part or all of the principal—especially Chapter 7. A Licensed Insolvency Trustee in Canada notes bankruptcy’s cost is not based on how much you owe (unlike a DMP), and that “bankruptcy is almost always less costly than a debt management plan, but the cost‑benefit is even greater the more you owe.”

Big caveat: Debt Management Plan vs Bankruptcy; Bankruptcy can trigger indirect “costs”—harder to rent, higher security deposits, potentially more expensive insurance, and impact on certain jobs. Those aren’t in the official fee, but they’re real financial impacts.

3. Debt Management Plan vs Bankruptcy; Which damages credit less?

Time on your credit report (U.S.)

- Bankruptcy:

- Chapter 7: Generally remains on your credit report for up to 10 years from the filing date.

- Chapter 13: Usually stays for up to 7 years from the filing date.

- Debt Management Plan:

- There is no fixed, multi‑year “bankruptcy clock.” Instead:

- Accounts in a DMP may be noted as being in a debt management/repayment plan.

- You may have to close the included credit card accounts, which can reduce your average age of accounts and increase your credit utilization initially—both of which can lower your score.

- However, NFCC notes that past missed payments may be removed from your credit reports as part of the arrangement, and that the long‑term impact to credit scores is generally positive because you’re paying down debt.

- As you complete the plan and reduce balances, your credit can steadily improve—there’s no 7‑ or 10‑year “bankruptcy” line dragging you down.

- There is no fixed, multi‑year “bankruptcy clock.” Instead:

Severity and perception

- Bankruptcy is viewed as a severe negative event by lenders. It indicates you could not repay your debts and needed legal relief. NFCC lists “major negative impact on your credit scores” and difficulty obtaining loans/cards for several years as cons of bankruptcy.

- DMP is less severe than bankruptcy in lenders’ eyes because:

- You are repaying what you owe (often at lower interest), not discharging debt.

- Nonprofit counseling organizations emphasize DMPs as a way to reduce interest and simplify payments “without the long‑term consequences of bankruptcy.”

- NFCC’s DMP pros explicitly highlight that the long‑term impact to credit scores tends to be positive once you’re on the plan and paying down debt, even if there is a short‑term dip when accounts close.

In Canada/UK, a similar pattern exists: A DMP may be coded as an R7 rating, while bankruptcy is an R9—R9 is considered worse. Debt Management Plan vs Bankruptcy; But experts stress that credit impact alone should not be the deciding factor; the math and your ability to pay matter more.

Score drop vs recovery

- Both paths can cause an initial score drop:

- Bankruptcy: Big drop due to the bankruptcy filing and any prior delinquencies.

- DMP: Initial drop can occur due to closing accounts and any prior late payments; then recovery as on‑time payments accumulate and balances fall.

- Recovery after bankruptcy: The impact lessens over time, especially if you use credit carefully afterward, but the public record and long reporting window mean many lenders remain cautious for years.

- Recovery after DMP: Because you’re paying in full and improving your debt‑to‑income ratio, many people see scores recover as they progress through the plan. The long‑term impact is often positive.

Net: Debt Management Plan vs Bankruptcy; DMP is clearly “less damaging” to your credit profile and to your future options than bankruptcy, if you can complete it.

4. Non‑credit differences you must weigh

Debt Management Plan vs Bankruptcy; These are often more important than the credit score difference alone.

Legal protection and certainty

- Bankruptcy:

- Automatic stay stops collection calls, lawsuits, and wage garnishments as soon as you file.

- Court‑supervised process; creditors must participate and cannot opt out.

- Discharge is legally binding—if the court discharges a debt, the creditor is legally barred from trying to collect it.

- DMP:

- Participation by creditors is voluntary. Some may choose not to, and they can still sue or garnish you (though many may agree to halt collection if you’re in the plan).

- No court order protects you; it’s an agreement, not a shield.

What debts can be included

- DMP:

- Generally: credit cards and some unsecured personal loans/utility bills.

- Usually excluded: student loans, secured loans (mortgage, auto), tax debts, some payday lenders, and certain legal debts.

- Bankruptcy (U.S.):

- Can wipe out or restructure most unsecured debts (credit cards, medical bills, many personal loans).

- Certain obligations survive: alimony/child support, many student loans (though some relief programs exist), recent tax debts, fraud‑related debts, and secured debts if you want to keep the collateral (you must keep paying the mortgage or car loan to avoid repossession/foreclosure).

Timeline to completion

- DMP:

- Typical duration: 3–5 years (36–60 months).

- You’re committing to a fixed monthly payment during that window.

- Bankruptcy:

- Chapter 7: Often resolved in a few months, plus whatever time it takes to sell nonexempt assets, if any. nerdwallet

- Chapter 13: 3–5 year repayment plan, similar in length to a DMP but with legal discharge at the end.

Public record and privacy

- Bankruptcy:

- It’s a public court filing. Anyone who searches court records can see it (though these days, mostly accessed professionally).

- It appears on your credit report for 7–10 years.

- DMP:

- Not a court filing, so there’s no public bankruptcy record.

- Creditors may note that you’re in a DMP, but it’s far less visible to the general world.

5. 2026 trends that matter to your choice

- Bankruptcy filings are rising: In the U.S., total filings for the 12 months ending Dec 31, 2025 reached 574,314—up 11% from the prior year—meaning more households are using bankruptcy again as a tool.

- Interest rates have been high: That increases the value of DMPs (which can lower card rates) and pushes some people toward bankruptcy when payments become unsustainable.

- Fees and rules for Chapter 13 continue to be tweaked: Courts periodically adjust administrative fee structures and presumive attorney fee allowances; this can affect what you pay in a Chapter 13 plan, but not the basic pros/cons.

- Nonprofit DMPs remain a primary alternative: Counseling agencies emphasize DMPs as a way to “pay off all credit card debt” with lower interest and fee waivers while avoiding bankruptcy’s long‑term consequences.

6. How to choose between them in 2026

Debt Management Plan vs Bankruptcy; Use these practical checkpoints.

Choose a DMP if:

- You can pay 100% of your unsecured debts in roughly 3–5 years with a realistic budget (especially if interest is lowered).

- Your debts are mostly credit cards and similar unsecured obligations that DMP providers can work with.

- You do not need immediate court protection from lawsuits or wage garnishment.

- You want to avoid the long‑term, heavy credit damage and public record of bankruptcy.

- You’re willing to close credit card accounts and live on a strict cash/budget plan for several years.

Choose bankruptcy (and consult a bankruptcy attorney) if:

- Even with reduced interest, there is no realistic way to repay your debts within 3–5 years.

- You’re being sued, your wages are being garnished, or creditors are escalating legal action—you need the automatic stay and legal protection.

- Your debts include obligations not typically handled by DMPs (e.g., substantial older tax debts, certain types of loans), and/or the amount is simply too high relative to your income.

- You’re okay with a major, multi‑year negative mark on your credit (up to 10 years for Chapter 7) in exchange for discharging debt and getting a fresh start.

Strongly recommended steps before you decide

- Talk with a nonprofit credit counseling agency (NFCC member or similar) about a DMP and get a written budget/plan.

- Talk with a qualified bankruptcy attorney for a free/low‑cost consultation to see whether you qualify for Chapter 7 or 13, and what a repayment plan would look like.

- Compare both:

- DMP: Total paid = principal + reduced interest + DMP fees.

- Bankruptcy: Attorney/filing fees + trustee payments (Chapter 13) OR mostly attorney/filing (Chapter 7), balanced against how much debt is discharged.

- Factor in non‑money costs: stigma (if relevant to your career), privacy, and future borrowing needs.

Bottom line

- A Debt Management Plan (DMP) usually damages your credit less than bankruptcy and lets you pay what you owe on better terms, but it doesn’t reduce principal. Debt Management Plan vs Bankruptcy; If you can genuinely afford to pay in full within about five years and don’t need the legal shield of bankruptcy, a DMP is often the better, lower‑damage path.

- Bankruptcy can save you far more money when you’re truly over‑your‑head, because it can discharge a large portion of your debts. Debt Management Plan vs Bankruptcy; The tradeoff is a serious, long‑term credit hit (up to 10 years for Chapter 7) and a public court record, but for many people it’s the only realistic way to regain financial stability.

Debt Management Plan vs Bankruptcy; If you’d like, you can share rough numbers (total unsecured debt, types of debts, and rough monthly income/expenses), and I can walk through which option tends to make more math sense in your situation—and what to ask a counselor or attorney to confirm.