Discover MVA (Market Value Added)—the key metric showing company value beyond capital. Learn how MVA drives growth & investor returns. Click to explore!

Learn, Explain What is MVA (Market Value Added)?

Discover what Market Value Added (MVA) is and how it measures a company’s value creation. Understand its importance for investors and business growth.

Economic Value Added (EVA) is aimed to be a measure of the wealth of shareholders. According to this theory, earning a return greater than the cost of capital increase value of company while earning less than the cost of capital decreases the value. For listed companies, Stewart defined another measure that assesses if the company has created shareholder value or not. Also Learned, EVA, What is MVA (Market Value Added)?

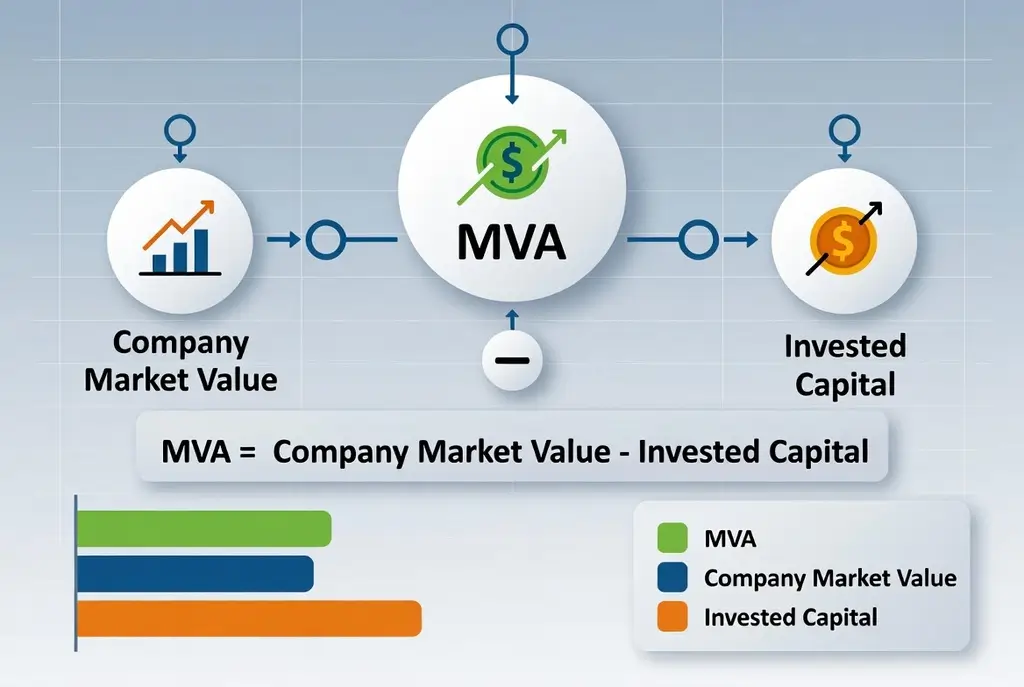

If the total market value of a company is more than the amount of capital invested in it, the company has managed to create shareholder value. However, if market value is less than capital invested, the company has destroyed shareholder value. The difference between the company’s market value and book value is called Market Valued Added or MVA.

From an investor’s point of view, Market Value Added (MVA) is the best final measure of a Company’s performance. Stewart states that MVA is a cumulative measure of corporate performance and that it represents the stock market’s assessment from a particular time onwards of the net present value of all a Company’s past and projected capital projects.

MVA is calculated at a given moment, but in order to assess performance over time, the difference or change in MVA from one date to the next can be determined to see whether the value has been created or destroyed.

The Market Value Added (MVA) measure is based on the assumption that the total market value of a firm is the sum of the market value of its equity and the market value of its debt. Stewart defines Market Value Added (MVA) as the excess of market value of capital (both debt and equity) over the book value of capital.

MVA (Market Value Added) Formula

Simply stated, Market Value Added (MVA) = Market value of the company – Capital invested in the company

Where,

- Market value: For a public listed company it is calculated as the number of shares outstanding x share price + book value of debt (since the market value of debt is generally not available). In order to calculate the market value of a firm, we have to value the equity part at its market price on the date the calculation is made. The total investment in the Company since day one is then calculated as the interest-bearing debt and equity, which includes retained earnings. Present market value is then compared with total investment. If the former amount is greater than the latter, the Company has created wealth.

- Capital invested: It is the book value of investments in the business made up of debt and equity.

Effectively, the formula becomes, Market Value Added (MVA) = Market value of equity – Book value of equity

According to Stewart,

Market Value Added (MVA) tells us how much value company has added to or subtracted from its shareholder’s investments. Successful companies add their MVA and thus, increase the value of capital invested in the company. Unsuccessful companies decrease the value of capital originally invested in the company. Whether a company succeeds in creating MVA (increasing shareholder value) or not, depends on its rate of return.

If a company’s rate of return exceeds its cost of capital, the company will sell on stock markets with premium compared to the original capital and thus, have positive MVA. On the other hand, companies that have the rate of return smaller than their cost of capital, sell with discount compared to the original capital invested in the company.

Market Value Added (MVA) is a cumulative measure of corporate performance and that it represents the stock markets assessments from a particular time onwards of the net present value of all of a Company’s past and projected capital projects. The disadvantage of the method is that like EVA there can be a number of value-based adjustments made in order to arrive at the economic book value and that it is affected by the volatility from the market values since it tends to move in tandem with the market.

Leave a Reply