Chapter 7 vs Chapter 13 Bankruptcy: Learn the critical difference between Chapter 7 and Chapter 13 bankruptcy — eligibility, timelines, and what happens to your assets.

Chapter 7 vs Chapter 13 Bankruptcy: Which Should You File?

Big picture;

- Chapter 7 is a “liquidation” case: quick (typically 3–6 months), you must pass the “means test,” and non-exempt assets can be sold to pay creditors. Most unsecured debts are wiped out at the end.

- Chapter 13 is a “repayment plan” for people with regular income: you keep your property and pay into a 3–5 year plan. You must be under debt limits and have enough income to fund the plan.

- Choose Chapter 7 if: your income is low enough to pass the means test, you have little non‑exempt equity, and you want the fastest possible fresh start.

- Choose Chapter 13 if: you’re behind on a mortgage or car loan and want to catch up, you have assets/excess equity you want to protect, your income is too high for Chapter 7, or you need tools only Chapter 13 provides (like lien stripping).

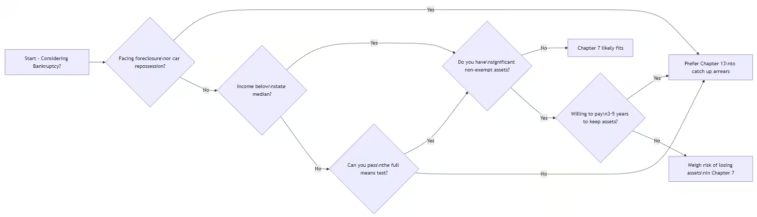

Chapter 7 vs Chapter 13 Bankruptcy: Below is a decision flow to visualize the typical choice (this isn’t legal advice, just a practical framework):

1. Core differences at a glance

| Feature | Chapter 7 (Liquidation) | Chapter 13 (Repayment) |

|---|---|---|

| What it is | Trustee may sell non‑exempt assets to pay creditors; most remaining unsecured debts are discharged. | You propose a 3–5‑year payment plan using your “disposable income”; you keep your property if you complete the plan. |

| Typical timeline | Discharge usually about 4 months; cases commonly close in 3–6 months. | Plan length: 3 years if your current monthly income is below your state median; generally 5 years if above. Discharge occurs after you complete all payments. |

| Eligibility – income | Must pass the means test (or qualify under exceptions). If your income is below the state median for your household size, you typically pass the first step. If above, allowed deductions and expense standards determine whether Chapter 7 is presumed abusive. | No formal “means test,” but you must have “regular income” to fund a plan. The same median income data determines whether your plan must be 3 or 5 years. |

| Eligibility – debt limits | None (you can file regardless of debt amount). | Yes: for cases filed April 1, 2025–Mar 31, 2028, you must have under $526,700 in unsecured debts and under $1,580,125 in secured debts on the filing date. |

| Your assets/exemptions | Exempt property is protected; non‑exempt property can be sold. Many states opt out of federal exemptions, so what’s exempt depends on your state’s law. | You typically keep all property while you make plan payments. Secured creditors keep their liens; you pay what’s required to keep collateral (e.g., catch up mortgage arrears, pay car loans). |

| Secured debts (home/car) | Liens survive. You can choose to “reaffirm” a debt and keep the asset, but if you’re behind, Chapter 7 doesn’t let you force a catch‑up plan. | Designed to help you catch up on missed mortgage payments and keep your home; you can also restructure some secured debts over the life of the plan. |

| Discharge timing | Generally about 4 months after filing (60 days after the first date set for the meeting of creditors, assuming no objections). | Upon successful completion of all plan payments—commonly around 4 years after filing for a 3–5 year plan. |

| Credit report | Bankruptcies may be reported for up to 10 years from the filing date; many consumer guides note Chapter 7 appears for up to 10 years. | Bankruptcies may be reported for up to 10 years as well, but many consumer sources describe Chapter 13 as commonly reported for up to 7 years. Practices can vary by bureau. |

| When it’s preferred | Low income, little non‑exempt equity, priority on speed and eliminating unsecured debts. | Need to stop foreclosure/catch up on a mortgage, protect non‑exempt equity, or you’re above the means test but can afford a 3–5‑year plan. |

2. Eligibility: Who can file which chapter?

Chapter 7 eligibility

- Who can file: Individuals, partnerships, corporations, or other business entities. For individuals, relief is available regardless of the amount of debt or whether you’re insolvent—subject to the means test and other bars.

- Means test basics:

- Applies to individual debtors whose debts are “primarily consumer” (not mainly business).

- First step: compare your “current monthly income” (annualized) to the state median income for your household size. The U.S. Trustee Program publishes these tables; for example, the Nov 1, 2025–Mar 31, 2026 table lists 1‑earner/4‑person median incomes by state.

- If your income is below the state median: you generally pass the first step and can proceed (unless other issues arise).

- If your income is above the state median: you complete the full means test using IRS-allowable expense standards and actual secured debt payments. If, after those deductions, your projected disposable income over five years exceeds statutory thresholds ($10,275 or 25% of non‑priority unsecured debts, whichever is greater; or a higher amount under the statute), Chapter 7 is presumed abusive.

- A presumption of abuse can be rebutted with “special circumstances” justifying additional expenses or income adjustments.

- Credit counseling requirement:

- You must complete an approved credit counseling briefing within 180 days before filing (with limited emergency/insufficient-agency exceptions). Chapter 7 vs Chapter 13 Bankruptcy: Any debt repayment plan developed during counseling must be filed.

- Prior-bankruptcy bars:

- If a prior case was dismissed in the last 180 days for willful failure to appear or comply with court orders, or was voluntarily dismissed after creditors sought relief from the stay, you’re generally barred from filing.

Chapter 13 eligibility

- Who can file:

- Individuals with regular income, including those who are self‑employed or operating an unincorporated business. Chapter 7 vs Chapter 13 Bankruptcy: Corporations and partnerships cannot use Chapter 13.

- Debt limits (current 2025–2028 cycle):

- As of filing date: unsecured debts must be less than $526,700; secured debts must be less than $1,580,125. These limits apply to cases filed April 1, 2025 through March 31, 2028.

- Income and plan length:

- You must propose a plan paying all “disposable income” over an “applicable commitment period.”

- If your current monthly income is below your state median for your household size, the commitment period is generally 3 years (court may approve longer “for cause”). If above median, it’s generally 5 years; plans cannot exceed 5 years.

- Credit counseling requirement:

- Like Chapter 7, you must complete approved credit counseling within 180 days before filing (with the same exceptions).

- Prior-bankruptcy discharge timing:

- Ineligible for a Chapter 13 discharge if you received a discharge in Chapter 7, 11, or 12 within 4 years before filing, or in a prior Chapter 13 within 2 years before filing.

Repeat-discharge rules (Chapter 7 after prior case)

- Second Chapter 7: denied if you received a Chapter 7 or 11 discharge within 8 years before the new filing.

- Chapter 7 after Chapter 12 or 13: denied if the prior case was filed within 6 years, unless you paid all allowed unsecured claims in full, or you paid at least 70% of allowed unsecured claims in a plan proposed in good faith and representing your best effort.

3. What happens to your assets?

Chapter 7: exemptions and liquidation risk

- The trustee administers a “bankruptcy estate” that becomes the temporary legal owner of most of your property as of the filing date.

- Exempt vs non‑exempt:

- You may protect “exempt” property under federal bankruptcy exemptions or your state’s exemption scheme; many states have “opted out” of the federal exemptions, so which set applies depends on where you live.

- The trustee liquidates non‑exempt assets and distributes proceeds to creditors. If all assets are exempt or fully encumbered by liens, the trustee typically files a “no asset” report and unsecured creditors receive nothing.

- Common examples:

- Often protected (depending on your state): a modest amount of home equity, a car up to a certain value, necessary household goods, tools of the trade, retirement accounts (e.g., 401(k), IRA). These protections vary significantly by state.

- Potentially at risk: substantial home equity beyond the exemption, a second car with significant equity, valuable collections, stocks/bonds outside protected accounts, tax refunds (in many jurisdictions). Whether and how much is at risk depends on local exemptions and trustee practice.

- Secured creditors:

- Liens (mortgages, car loans) survive Chapter 7. You can choose to “reaffirm” and keep the collateral, redeem it by paying its lump‑sum value, or surrender it. A discharge wipes out personal liability, but not the lien.

Chapter 13: keeping property while paying into a plan

- You generally keep all your property, but you must pay enough to satisfy certain requirements:

- Secured creditors: to keep collateral (e.g., house or car), the plan must pay at least the allowed value of the collateral (or, for certain recent purchase‑money debts, the full debt). Chapter 7 vs Chapter 13 Bankruptcy: Mortgages can be cured over the plan period while you stay current on new payments.

- Non‑exempt equity advantage:

- Because Chapter 13 is a repayment structure rather than a liquidation, you aren’t forced to sell non‑exempt assets; instead, your unsecured creditors must receive at least as much as they would have in a Chapter 7 liquidation.

- Tools unique to Chapter 13:

- Lien stripping: If your home’s value is less than what you owe on senior mortgages, junior liens (e.g., a second mortgage or HELOC) can be treated as wholly unsecured and “stripped” (removed) at plan completion. This option is only available in Chapter 13, not Chapter 7.

4. Timeline: how long does each case take?

Chapter 7 timeline (typical)

- File petition + schedules → automatic stay stops most collections.

- Meeting of creditors (§341 meeting): held roughly 21–40 days after filing (up to 60 days in some locations).

- Trustee’s means test report: filed within 10 days after the meeting.

- Discharge: typically granted about 60 days after the first date set for the §341 meeting if no objections or motions to dismiss are filed—roughly 4 months total.

- Closing: soon after discharge if the estate is “no asset,” or after asset administration if there are assets to distribute. Most individual Chapter 7s are “no asset” cases.

Chapter 13 timeline (typical)

- File petition (and usually a proposed repayment plan within 14 days) → automatic stay.

- Meeting of creditors: generally 21–50 days after filing (up to 60 days in some places).

- Confirmation hearing: no later than 45 days after the meeting of creditors; the court decides whether to confirm the plan.

- Plan payments: you start making payments to the trustee within 30 days of filing, even before confirmation. You pay monthly (or biweekly) for 3–5 years depending on income.

- Discharge: once you complete all plan payments and meet all other requirements (like financial management counseling), the court grants discharge.

5. Eligibility in practice: 2026 examples

Chapter 7 vs Chapter 13 Bankruptcy: These are illustrative; actual eligibility depends on your specific numbers and state law.

- Example 1: Chapter 7 likely fits

- Who: single person in Florida, household size 1, gross annual income $65,000 (no dependents).

- State median (Nov 1, 2025–Mar 31, 2026): 1‑earner/1‑person median in Florida is $68,085. Your income is below the state median, so you pass the first prong of the means test.

- Assets: older car with small equity, renter, no significant non‑exempt assets.

- Result: Chapter 7 likely feasible; talk to a lawyer to confirm exemptions and any local issues.

- Example 2: Chapter 13 preferred

- Who: married couple in California, two children, household size 4; gross annual income $160,000.

- State median: 4‑person median in California (Nov 1, 2025–Mar 31, 2026) is $135,505. Chapter 7 vs Chapter 13 Bankruptcy: You’re above median, so you must complete the full means test.

- After allowed IRS standard expenses and actual secured debt payments, your projected disposable income may be high enough that Chapter 7 is presumed abusive.

- Other facts: you’re behind on mortgage payments but want to keep the house; you have non‑exempt home equity.

- Result: Chapter 13 lets you catch up mortgage arrears and protect equity; Chapter 7 is riskier and may be barred by the means test.

- Example 3: Debt limits push toward Chapter 7 or 11/12

- Who: small business owner with significant personal guarantees; unsecured debts total $600,000 and secured debts $1,000,000.

- Chapter 13 debt limits: $526,700 unsecured and $1,580,125 secured. You’re above the unsecured cap, so you’re ineligible for Chapter 13.

- If you’re an individual, Chapter 7 remains available (no debt limits) subject to the means test. If you want to reorganize, Chapter 11 (or Chapter 12 if family farmer/fisherman) might be options.

6. Which should you file? Decision factors

Chapter 7 vs Chapter 13 Bankruptcy: Consider these questions with a local bankruptcy attorney:

- Are you facing foreclosure or repossession?

- Yes, and you want to keep the house/car: Chapter 7 vs Chapter 13 Bankruptcy: Chapter 13 is usually the better tool to stop foreclosure and catch up arrears over time.

- Is your income relatively low?

- If your income is below your state median and you have little non‑exempt equity, Chapter 7 is often the fastest and least expensive path to a discharge.

- Do you have significant non‑exempt equity?

- If your equity in a home, car, or other assets exceeds what exemptions protect, Chapter 7 may risk losing those assets or may require you to pay to “buy back” non‑exempt value. Chapter 13 can protect that equity as long as your plan pays unsecured creditors at least as much as they’d get in a Chapter 7 liquidation.

- Do you need tools like lien stripping?

- If you owe more on your first mortgage than your home is worth, and you have a second mortgage or HELOC, Chapter 7 vs Chapter 13 Bankruptcy: Chapter 13 can strip that junior lien at plan completion. Chapter 7 does not provide this option.

- Have you recently received a bankruptcy discharge?

- Got a Chapter 7 discharge less than 8 years ago? You likely won’t get another Chapter 7 discharge. Chapter 13 might be an option sooner (4 years from a prior Chapter 7, 2 years from a prior Chapter 13).

- Got a Chapter 13 discharge less than 2 years ago? You likely won’t get another Chapter 13 discharge yet. Chapter 7 may be possible depending on timing and earlier plan payments.

- How important is speed vs. control?

- Speed priority: Chapter 7 usually concludes within months.

- Control and asset protection priority: Chapter 13 lets you stretch and reorganize debts over 3–5 years while keeping property.

7. Credit reporting and long-term impact

- Fair Credit Reporting Act (FCRA) allows credit bureaus to report a bankruptcy for up to 10 years from the filing date.

- Consumer guides typically summarize:

- Chapter 7: reported for up to 10 years.

- Chapter 13: often reported for up to 7 years.

- In practice, both chapters can significantly lower scores at first, but many people begin rebuilding credit soon after filing by using secured cards, on‑time payments, and keeping balances low.

8. Key non-dischargeable debts (both chapters)

Chapter 7 vs Chapter 13 Bankruptcy: Both chapters have similar “non-dischargeable” debts; the discharge doesn’t eliminate them, and Chapter 13 may require you to pay some in full. Common categories include:

- Most domestic support obligations (child support, alimony).

- Most tax debts (with exceptions; some older income taxes can be discharged).

- Student loans (unless you can show “undue hardship” in a separate adversary proceeding).

- Debts from fraud, willful and malicious injury, certain DUI-related liabilities, and certain other specific types.

9. What you should do next

- Gather your numbers: last 6 months of income, major expenses, secured and unsecured debt balances, and asset values.

- Check your state’s exemption scheme and the latest median income figures for your household size (DOJ publishes updated tables periodically).

- Talk with a local bankruptcy attorney—means test calculations, exemptions, and lien-stripping analyses are state‑specific and fact‑intensive; a lawyer can run the numbers and recommend whether Chapter 7, Chapter 13, or a non‑bankruptcy alternative is best for you.

Chapter 7 vs Chapter 13 Bankruptcy: This guide reflects current law and 2025–2026 data (including Chapter 13 debt limits and median income tables), but courts and local practices vary, and laws can change. Use this as a foundation, not a substitute for personalized legal advice.

Leave a Reply