Filing bankruptcy without an attorney costs $300–$400, but mistakes can cost thousands. How to File for Bankruptcy; This guide covers Chapter 7 vs 13 eligibility, the means test, exemptions, and discharge timelines for 2026.

How to File for Bankruptcy in 2026: Chapter 7 vs 13, Costs & What Happens to Your Assets

How to File for Bankruptcy? Great question—and it’s one where a little preparation up front can save you a lot of money and stress.

Short answer (2026 snapshot)

- If your income is low and you don’t have much equity in property, Chapter 7 is usually the faster, cheaper way to wipe out unsecured debts—but the trustee can sell non‑exempt assets to pay creditors. How to File for Bankruptcy; You typically keep only “exempt” property (e.g., basic home equity up to a state limit, an inexpensive car, retirement accounts, clothing, furnishings).

- If you have regular income, are behind on a mortgage or car, and/or you have non‑exempt property you don’t want to lose, Chapter 13 is usually the better fit: you keep everything but you must pay into a 3– to 5‑year repayment plan (and any non‑exempt equity is effectively “paid back” through those plan payments).

- Costs in 2026: federal court filing fees are $338 for Chapter 7 and $313 for Chapter 13; most people also pay attorney fees (often in the $1,000–$6,000 range for Chapter 13, commonly less for a simple Chapter 7).

- As soon as either chapter is filed, the “automatic stay” takes effect: it stops most collections, lawsuits, wage garnishments, and foreclosure/repossession actions immediately (unless a creditor gets the stay lifted later).

How to File for Bankruptcy; Below is a clear 2026 roadmap: how eligibility works, step‑by‑step filing, costs, and exactly what happens to your assets in each chapter.

Big picture: how Chapter 7 and 13 differ (in plain language)

- Chapter 7 = “Liquidation”

- Purpose: Get rid of eligible unsecured debts quickly (typically about 3–6 months).

- Who it’s for: People whose current monthly income is below the state median for their household size, after allowed expenses, or who still qualify after detailed “means test” calculations.

- What happens to assets: You keep exempt property (protected by your state’s exemptions or, in some states, federal exemptions). How to File for Bankruptcy; Anything “non‑exempt” can be sold by the Chapter 7 trustee to pay creditors.

- Chapter 13 = “Repayment”

- Purpose: Catch up on secured debts (mortgage, car) and pay what you can on unsecured debts over 3–5 years; at the end, most remaining unsecured debts are discharged.

- Who it’s for: Individuals with regular income who don’t pass the Chapter 7 means test OR who have non‑exempt assets they want to keep or overdue mortgage/car payments they need to cure.

- What happens to assets: You keep all of your property (exempt and non‑exempt). How to File for Bankruptcy; You must pay unsecured creditors at least as much as the value of your non‑exempt assets through your repayment plan.

Here’s a decision flow in visual form:

Who can file Chapter 7 vs Chapter 13 (2026 rules)

- Chapter 7 eligibility:

- Must pass the “means test”: In general, your average monthly income for the 6 full months before filing must be lower than the median income for a household of your size in your state. How to File for Bankruptcy; If it’s higher, you do a second part of the test that deducts allowed expenses to see if you still qualify. Forms 122A‑1 (Chapter 7) and 122C‑1 (Chapter 13) use the Census/IRS/CLI data published each year by the U.S. Trustee Program for these calculations.

- There are also debt limits: you generally cannot have more than about $1,580,125 in secured debts and about $526,700 in unsecured debts (these amounts adjust periodically).

- Chapter 13 eligibility:

- Must be an individual (or husband and wife) with regular income.

- Your unsecured debts must be under about $526,700 and secured debts under about $1,580,125 (as of 2026).

- You propose a 3– to 5‑year repayment plan using all of your “disposable income” (what’s left after allowed expenses) to pay creditors; the plan must be feasible and proposed in good faith.

Note: If you don’t pass the Chapter 7 means test, Chapter 13 is usually the next option to consider—but a lawyer can also analyze whether there are other avenues or whether your situation might still fit Chapter 7 under the detailed calculations.

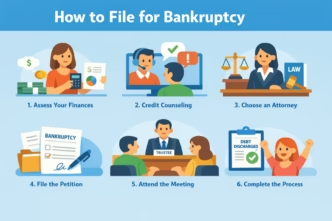

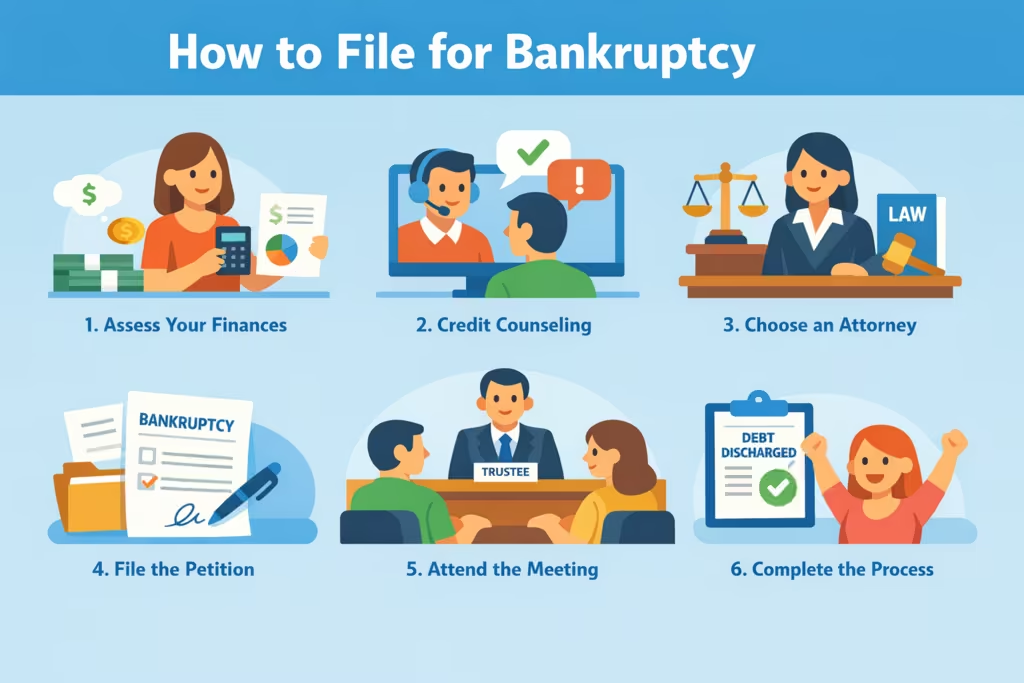

Step 1: Before you file – mandatory prep (both chapters)

- Get credit counseling from an approved agency (before filing):

- You must complete a briefing from an approved nonprofit credit counseling/debtor education agency within 180 days before filing (unless the court waives this for exigent circumstances).

- Typical cost: around $10–$50 per course; sometimes waived if your income is very low.

- Gather documents:

- Proof of income: pay stubs for the last 6 months, W‑2s or tax returns.

- Asset documents: property deeds, auto titles, registration, account statements.

- Debt listing: recent statements for all debts (mortgages, car loans, credit cards, medical bills, personal loans).

- ID: driver’s license, Social Security number.

- Decide which chapter fits your goals:

- Want to get out of debt quickly and don’t mind losing non‑exempt property? → leans Chapter 7.

- Need to protect a house or car from foreclosure/repossession, or you have equity you’d rather “pay back” than lose? → leans Chapter 13.

Step 2: How to actually file (both chapters)

Consult a bankruptcy lawyer (strongly recommended):

- The law lets you file “pro se” (without an attorney), but most people have better outcomes with a lawyer, especially in Chapter 13 or any Chapter 7 with complications (recent asset transfers, business debts, disputes).

File the petition:

- Your lawyer (or you, if pro se) files:

- Voluntary petition (official form asking for bankruptcy relief),

- Schedules listing your:

- Income and expenses,

- All assets and their values,

- All debts and creditors,

- Any leases or contracts.

- For Chapter 7: Form 122A‑1 (Statement of Current Monthly Income) for the means test.

- For Chapter 13: Forms 122C‑1 and 122C‑2 to calculate current monthly income and disposable income for your repayment plan.

Pay the filing fee (and request a waiver or installments if needed):

- 2026 filing fees (federal):

- Chapter 7: $338 total (includes $245 filing fee + $78 administrative fee + $15 trustee surcharge).

- Chapter 13: $313 total (includes $236 filing fee + $78 administrative fee).

- If your income is below 150% of the federal Health and Human Services Poverty Guidelines, you can apply to have the filing fee waived (Form B103B). The court can also let you pay the fee in up to four installments for Chapter 7.

Get your case number and the automatic stay:

- As soon as the petition is filed, the court issues your case number.

- The automatic stay takes effect immediately, stopping:

- Most collection calls and letters,

- Wage garnishments,

- Lawsuits and foreclosure repossession activities,

- (Note: some actions like certain evictions or criminal proceedings can continue.)

Complete the financial management course (after filing):

- You must complete an approved debtor education financial management course before you can receive a discharge. There’s a small course fee on top of any counseling fees.

Chapter 7 path: what happens, timing, and your assets

What Chapter 7 does

- Discharges most of your general unsecured debts (credit cards, medical bills, personal loans) if you qualify and complete the process.

- Secured debts (mortgage, car loan) are NOT discharged—creditors keep their lien on the house or car; if you’re behind, they can pursue foreclosure/repossession after the stay lifts or, in some cases, during the case if they get relief from stay.

- Certain debts usually can’t be discharged:

- Most student loans (especially federal),

- Recent taxes,

- Child support and alimony,

- Debts from fraud,

- Criminal fines/restitution.

Typical timeline (Chapter 7)

- File petition and schedules → Automatic stop of collections →

- Trustee appointed and examines your papers under oath →

- Meeting of creditors (usually 20–40 days after filing) → Trustee asks you questions under oath; creditors rarely object in routine Chapter 7 cases →

- ~60–90 days after filing: Trustee and court decide if there are any “abuse” issues (luxury purchases, preferential payments, etc.) →

- If no major issues, court enters discharge order and eligible debts are wiped out.

What happens to your assets in Chapter 7

- Exempt property:

- You keep all property that’s protected by applicable exemptions:

- Often: a certain amount of home equity (“homestead”), a modest car, household goods and clothing, tools of the trade, most retirement accounts (up to statutory limits).

- Each state has its own exemption list; some states let you choose between state exemptions and federal “nonbankruptcy” exemptions. You cannot mix and match; you generally choose one system or the other.

- You keep all property that’s protected by applicable exemptions:

- Non‑exempt property:

- The trustee can take and sell non‑exempt property and distribute proceeds to creditors according to bankruptcy priority rules. This might include:

- A second vehicle,

- A vacation or investment property,

- Valuable collections (jewelry, antiques) beyond exemption limits,

- Tax refunds or bank accounts beyond what’s exempt.

- “Presumption of abuse” rules: Large recent purchases of “luxury goods or services” or large cash advances before filing can be treated as abuse and may affect your case or the trustee’s actions.

- The trustee can take and sell non‑exempt property and distribute proceeds to creditors according to bankruptcy priority rules. This might include:

How to File for Bankruptcy; Key takeaway for Chapter 7 assets: You can often keep your main car, essential household goods, and often some home equity—but anything clearly non‑exempt can be sold for your creditors.

Chapter 13 path: what happens, timing, and your assets

What Chapter 13 does

- Sets up a court‑approved repayment plan (usually 36–60 months; commonly 3–5 years).

- You make one monthly payment to a trustee, who pays your creditors according to the plan.

- At the end of the plan, the court discharges most remaining unsecured debts that weren’t paid in full. Secured debts (mortgage, car) survive the plan; you must keep paying those to keep the collateral.

Typical timeline (Chapter 13)

- File petition and schedules (including Forms 122C‑1/122C‑2) → Automatic stay takes effect →

- About 30 days after filing: Start making plan payments to the trustee even if your plan is not yet officially confirmed. If you don’t start, the court can dismiss your case.

- About 45 days after filing: Meeting of creditors (same as Chapter 7). The trustee and creditors can raise objections to your plan; you may need to revise it.

- Before or soon after the creditors meeting: Plan confirmation hearing. Judge confirms or denies your plan; if confirmed, it binds you and your creditors.

- You make plan payments for 3–5 years → Complete all required payments and a post‑plan financial management course → Court issues discharge order for remaining eligible debts.

What happens to your assets in Chapter 13

- Exempt property:

- You keep it, same as in Chapter 7—exemptions don’t change between chapters.

- Non‑exempt property:

- You keep it—but you must pay unsecured creditors at least as much as the value of your non‑exempt assets through your Chapter 13 plan.

- That “value” is effectively what your disposable income can fund over 3–5 years.

- Extra tools in Chapter 13:

- “Lien stripping”: If a junior lien (like a second mortgage or lien that “impairs” an exemption on your home) qualifies, the court can remove (“strip”) it, treating the debt as unsecured and potentially discharging the balance at the end of your plan.

- “Cram down”: The plan can sometimes reduce the principal or interest on certain secured claims (other than your primary residence mortgage) to a collateral’s fair market value.

How to File for Bankruptcy; Key takeaway for Chapter 13 assets: You keep everything, but the price you pay is higher over time because you’re effectively “buying back” the value of non‑exempt assets through your plan payments.

Costs: what you’ll actually pay in 2026

Court filing fees (nationwide):

- Chapter 7:

- $338 total (includes $245 filing fee, $78 administrative fee, $15 trustee surcharge).

- Chapter 13:

- $313 total (includes $236 filing fee, $78 administrative fee).

Fee waivers and installment options:

- If your income is below 150% of the federal HHS Poverty Guidelines, you can apply to have the Chapter 7 filing fee waived (Official Form B103B).

- For Chapter 7, many courts allow you to pay the filing fee in up to four installments within 120 days (e.g., four installments of roughly $80–$100, with a final slightly larger payment).

- Chapter 13 filing fee cannot be paid in installments by law (unlike Chapter 7).

Mandatory credit counseling and debtor education:

- Pre‑filing credit counseling briefing: usually $10–$50 (may be waived if you’re indigent).

- Post‑filing financial management course: another small fee. Required to get your discharge.

Attorney fees:

- Chapter 7 attorney fees: Many lawyers quote flat or low four‑figure fees for a routine Chapter 7. How to File for Bankruptcy; Complex cases (business debts, asset disputes, recent transfers) cost more.

- Chapter 13 attorney fees: Commonly range around $4,000–$6,000 in 2026, because the case is more work: the lawyer must propose a feasible plan, handle objections, and attend confirmation hearings over a multi‑year period.

- Courts and many attorneys offer payment plans for attorney fees—but that’s separate from the court filing fee.

Rough total (ballpark):

- Simple Chapter 7: filing fee ($338) + counseling/education (under ~$100) + attorney (e.g., $1,500) → roughly around $2,000+ all‑in.

- Chapter 13: filing fee ($313) + counseling/education (~$100) + attorney (e.g., $4,000–$6,000) → roughly around $4,500–$6,500+ over 3–5 years.

Your house and car: how Chapter 7 vs 13 treats them

- House (primary residence):

- Chapter 7:

- You keep your house if:

- You’re current on the mortgage,

- You can protect all your equity with an applicable homestead exemption, and

- You can keep making payments. The lender keeps its mortgage lien; bankruptcy doesn’t erase that debt. If you’re behind, the lender can seek relief from the automatic stay to pursue foreclosure after the case ends or ask the court to lift the stay.

- You keep your house if:

- Chapter 13:

- Often better if you’re behind on mortgage or have equity that’s not fully exempt:

- Repayment plan can let you catch up on arrears (missed payments) over 3–5 years.

- You can also “strip” qualifying junior liens that impair exemptions.

- Often better if you’re behind on mortgage or have equity that’s not fully exempt:

- Chapter 7:

- Car:

- Chapter 7:

- If the car’s equity is within your state’s motor vehicle exemption, you can typically keep the car (as long as you stay current on loan payments).

- If equity is above the exemption, the trustee may sell the car, give you the exempt amount, and pay the remainder to your car lender (or you may pay the difference to keep the car).

- Chapter 13:

- You keep the car as long as your plan pays the entire car loan over time (and any arrears).

- Chapter 7:

Debts that usually survive both chapters

How to File for Bankruptcy; These are typically NOT discharged (you still have to pay):

- Most student loans (especially federal student loans),

- Child support and alimony,

- Most tax debts (some very old taxes can be dischargeable under strict rules),

- Criminal restitution and fines,

- Secured debts (mortgages, car loans) where you keep the collateral—these liens survive and you must keep paying if you want to keep the house/car.

How long each stays on your credit report

- Chapter 7:

- Remains on your credit report for up to 10 years from filing. However, its impact on your score typically lessens over time as you rebuild credit.

- Chapter 13:

- Remains on your credit report for up to 7 years from filing. Like Chapter 7, its scoring impact fades with responsible credit use afterward.

Common 2026 pitfalls to avoid

- Waiting too long: Bankruptcy filings were up about 11% in the 12 months ending December 31, 2025—you’re not the only one considering it. How to File for Bankruptcy; Acting earlier can stop garnishments sooner and protect assets sooner.

- Running up balances on credit cards or taking large cash advances right before filing:

- Debts for “luxury goods or services” or large cash advances before filing may be treated as abuse under the “presumption of abuse”/totality doctrines. How to File for Bankruptcy; Courts can dismiss your case or deny discharge of those debts.

- Selling or giving away assets for less than fair value before filing:

- The trustee can avoid certain transfers; lookbacks are possible and can complicate or prolong your case.

- Ignoring secured debts:

- Bankruptcy does not eliminate secured liens; if you want to keep the house or car, you must be able and willing to pay those loans moving forward. Chapter 13 is often built for that purpose.

How to choose between Chapter 7 and 13 (simple 2026 framework)

- Consider Chapter 7 first if:

- Your household income is below your state’s median (or close enough that you likely pass the means test), and

- Your debts are mostly unsecured (credit cards, medical, personal loans), and

- You don’t have much non‑exempt equity you’re desperate to keep (or you’re okay losing it), and

- You want the fastest fresh start.

- Consider Chapter 13 first if:

- Your income is regular and above the Chapter 7 means test, or

- You’re behind on your mortgage or car and want to catch up over time, or

- You have non‑exempt property (e.g., a vacation home, a second car with equity, investments) that you want to keep, or

- You have priority debts that must be paid in full (certain taxes, child support, etc.), and a structured 3–5 year plan will make that manageable.

- If anything is complicated or you’re not sure which path you’re on, talk with a local bankruptcy lawyer:

- Ask for a free or low‑cost consultation.

- Bring:

- A summary of your income and major expenses,

- A list of all debts (with balances and whether each is secured),

- A list of assets (with rough values),

- Any recent large financial transactions (e.g., gifts, asset sales, luxury purchases).

How to File for Bankruptcy; This guide reflects 2026 rules: median income data and means‑test forms for cases filed on/after April 1, 2026; filing fees of $338 (Chapter 7) and $313 (Chapter 13); and the same basic asset exemption framework as in recent years.

Leave a Reply