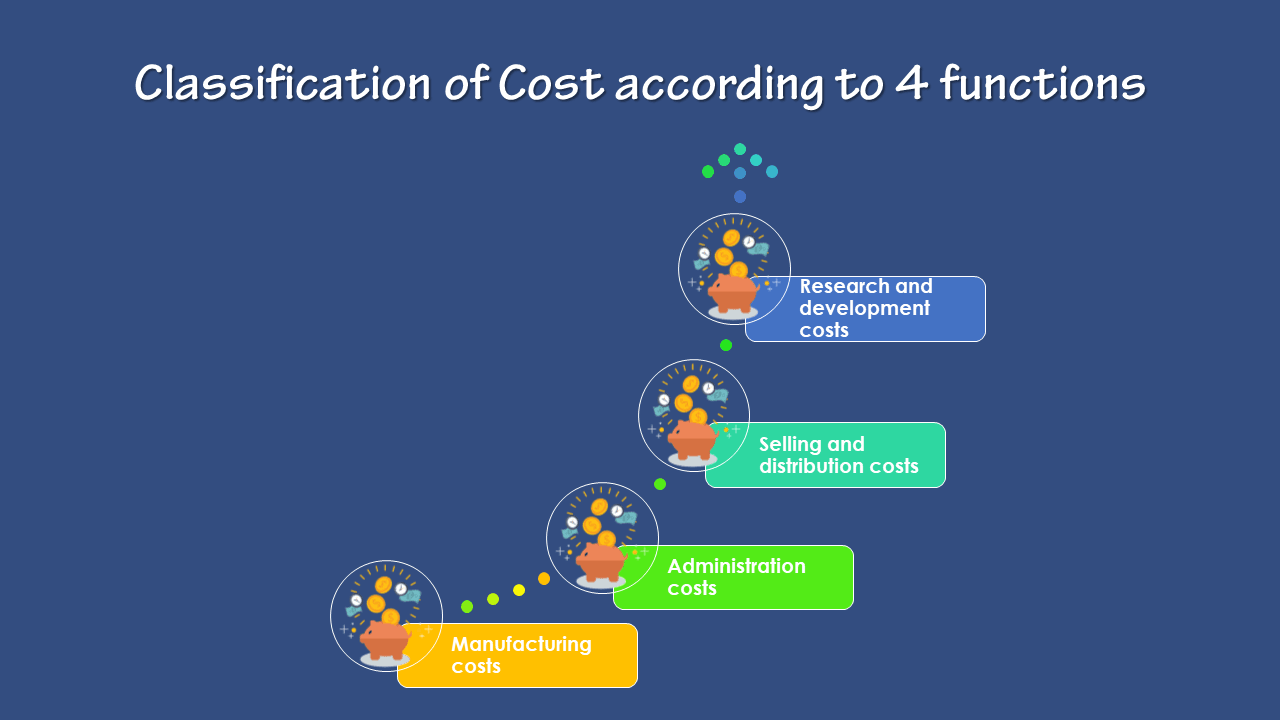

Classification of Cost according to 4 functions: This is a traditional classification. A business has to perform several functions like manufacturing, administration, selling, distribution, and research.

This article explains the topic of the Classification of Cost according to 4 functions.

Cost may have to ascertain for each of these functions.

On this basis, costs are classifying into the following groups:

Manufacturing costs:

This is the cost of the sequence of operations. Which begins with supplying materials, labor, and services and ends with the completion of production. What are the manufacturing costs? Manufacturing costs are the costs of materials plus the costs to convert the materials into products. Manufacturing costs are the costs incur during the production of a product.

The costs are typically present in the income statement as separate line items. An entity incurs these costs during the production process. Direct material is the materials uses in the construction of a product. Direct labor is that portion of the labor cost of the production process that assigns to a unit of production. Manufacturing overhead costs are applying to units of production based on a variety of possible allocation systems. Such as by direct labor hours or machine hours incurred.

Administration costs:

This is general administrative cost and includes all expenditure incurs in formulating the policy, directing the organization and controlling the operations of an undertaking. Which is not directly related to production, selling and distribution, research and development activity or function.

Define administrative costs as the costs not directly related to operations. Generally, they are incurring in the process of directing a company. These costs, though indirect, are still important because they assist those who operate and sell company products by making their work more efficient.

Selling and distribution costs:

Selling cost is the cost of seeking to create and simulating demand and securing orders. Distribution cost is the cost of a sequence of operations. This begins with making the packed product available for despatch and ends with making the reconditioned returned empty package for re-use. There are some overhead about them;

- What is Selling Overhead? Selling overhead is the indirect expenses incur for seeking to create and stimulate demand for the product and up to the stage of securing orders.

- What is Distribution Overhead? Distribution overhead is the expenses incurred in connection with the execution of an order. It begins with making the packed product available for dispatch and ends with making the reconditioned empty package, if any, available for re-use.

The various items included in manufacturing administrative, selling and distribution costs ate available in Table:

Research and development costs:

Research cost is the cost of searching for new or improved products or methods. It comprises wages and salaries of research staff, payments to outside research organizations, materials used in laboratories and research departments, etc. After completion of research, the management may decide to produce a new improved product or to employ a new or improved method.

Development cost is the cost of the process which begins with the implementation of the decision to produce a new product or to employ a new or improved method and ends with the commencement of formal production of that product or by that method. Pre-production cost is that part of the development cost which incurs in making in trial production run preliminary to formal production.

Leave a Reply