Payment gateway instant payout, Get paid instantly. Access your funds the moment a payment clears. Boost cash flow & grow your business. No more waiting.

📋 Payment gateway instant payout: 2026 Complete Guide

Payment gateway instant payout; Get instant payouts with our secure payment gateway—fast, reliable transactions in minutes. Boost cash flow today!

Here’s a complete 2026 guide to “instant payout” capabilities through payment gateways and PSPs: how they work, who offers what, what they cost, and how to choose and implement them.

Quick answer / TL;DR

- “Instant payout” means money moves from your payment gateway/PSP to your bank account (or your users’ accounts) in seconds/minutes instead of days.

- It’s usually:

- 1–3 business days by default for cards (standard settlement)

- 10 seconds via SEPA Instant in the EUecb.

- 24/7/365 over real-time rails like FedNow, RTP, SEPA Instant, UPI, PIX, etc.

- Major options:

- Card‑network instant payouts (Stripe, Adyen, PayPal, Square, etc.)

- Real‑time bank transfers (account‑to‑account via FedNow, RTP, SEPA Instant, Pay‑by‑Bank, UPI, PIX)

- Payout‑API platforms (Wise Platform, Airwallex, Dots, Trolley, Tipalti, Brite, Noda, etc.)

- Typical pricing: around 1–1.5% of the payout amount for card‑based instant payouts (e.g., Stripe 1.5% minimum 50¢; Square 1.5%; PayPal ~1.5%).

- Best fit if: you run a marketplace, gig platform, or any business where sellers/drivers/contractors expect to be paid immediately.

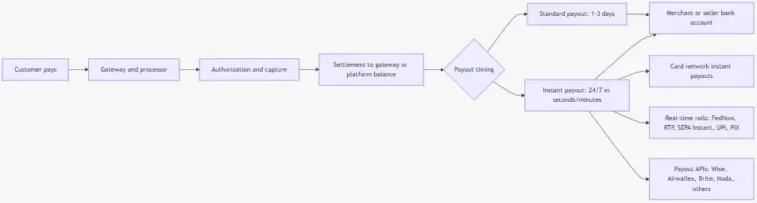

High‑level flow: what “instant payout” actually does

Payment gateway instant payout; This is the lifecycle when a customer pays and you (or your sellers) get paid instantly.

1. Concepts: settlement vs payouts vs instant payouts

Settlement vs payout vs instant payout

- Settlement:

- The gateway/processor moves funds from the customer’s bank/card issuer to your merchant balance.

- For cards, this is usually 1–3 business days after the transaction.

- Payout:

- Funds move from your merchant/platform balance to your (or your users’) bank account or card.

- Traditionally runs on batch schedules (e.g., daily T+2 or T+3).

- Instant payout:

- You trigger a payout that settles in seconds/minutes, 24/7/365, using:

- Card‑network instant rails (to a debit card), or

- Real‑time payment networks (e.g., FedNow, RTP, SEPA Instant, UPI, PIX).

- Example: Stripe Instant Payouts to an eligible debit card/bank “usually appear… within 30 minutes,” available weekends/holidays.

- You trigger a payout that settles in seconds/minutes, 24/7/365, using:

Real‑time payment rails that make instant payouts possible

- US:

- The Clearing House RTP network

- Federal Reserve FedNow Service (both launched and now broadly used for real‑time payments).

- EU/EEA:

- SEPA Instant Credit Transfer (SCT Inst): funds available in the payee’s account within 10 seconds, 24/7/365.

- New EU Instant Payments Regulation (IPR) is mandating broader availability and payee verification by 2025–2026.

- Other countries:

- UPI (India), PIX (Brazil), FPS (UK), NPP (Australia), etc., many with sub‑10 second settlement times.

- Real‑time APIs and orchestration layers (e.g., Lightspark Grid) route across these rails globally.

Payment gateway instant payout; Your gateway/PSP doesn’t always expose these directly, but instant payout products are usually built on top of them.

2. Typical use cases for instant payouts

Payment gateway instant payout; Instant payouts are most valuable when cash flow timing is a competitive or UX lever:

- Marketplaces & two‑sided platforms

- Pay sellers instantly after each order to attract and retain them (FedNow specifically highlights this use case).

- Gig & on‑demand platforms

- Ride‑sharing, delivery, task services — pay drivers/couriers instantly after shifts or individual jobs.

- Creator economy

- Pay creators/streamers instantly after tips or sales; improve loyalty and reduce churn.

- B2B supplier payments

- Enable suppliers to get paid on delivery instead of waiting weeks.

- Insurance claims & refunds

- Instant claim payouts or refund settlements improve customer satisfaction.

- SaaS with embedded finance

- Platforms embed instant payouts as a value‑added feature for their users (e.g., “get paid instantly” toggles).

Payment gateway instant payout; If your users don’t care strongly about same‑day access, standard payouts are usually cheaper and simpler.

3. How instant payout implementations usually work

Payment gateway instant payout; Two main patterns:

A) Merchant‑centric instant payout (you get paid faster)

- You accept payments via a gateway (Stripe, Adyen, Square, PayPal, etc.).

- Instead of waiting T+2/T+3 for standard settlement, you enable “Instant Payouts” or “Instant Transfers”:

- Funds go from your gateway balance to your bank account or debit card in minutes.

- You pay a fee (often ~1–1.5%) and there can be caps/limits.

B) Platform/payout‑API instant payout (you pay your users faster)

- You run a marketplace or gig platform.

- You use:

- Payout‑oriented products (Stripe Connect Instant Payouts, Adyen for Platforms, Wise Platform, Airwallex, Dots, Trolley, Brite, Noda, etc.).

- You call an API to trigger an instant payout to a user’s:

- Debit card (Visa/Mastercard), or

- Bank account via real‑time rails (FedNow, RTP, SEPA Instant, etc.).

- The PSP handles:

- Compliance and screening

- FX (if cross‑currency)

- Tracking and webhooks

- Reconciliation

Most “instant payout gateways” for platforms are really PSPs exposing a payout API + real‑time rails.

4. Major instant payout options (gateway/PSP level)

Payment gateway instant payout; Below is a practical, non‑exhaustive list as of 2025–2026.

1) Stripe Instant Payouts

- What it is:

- Move funds from your Stripe balance to an eligible debit card or bank account in minutes.

- Key facts:

- Funds “usually appear… within 30 minutes”; can request anytime, including weekends/holidays.

- Pricing (standard Stripe account): 1.5% of Instant Payouts volume, minimum fee 50¢.

- New users aren’t immediately eligible; eligibility is shown in the Dashboard.

- Different pricing/eligibility may apply under Stripe Connect for platforms.

- Best for:

- Online businesses in supported countries wanting fast access to operating cash.

- Platforms using Connect to offer instant payouts to sub‑merchants/users (where supported).

2) PayPal Instant Transfer

- What it is:

- Move your PayPal balance to a bank account or eligible card instantly instead of waiting days.

- Key facts:

- Instant transfers typically cost about 1.5% of the transferred amount, with minimum fees based on currency.

- Standard bank withdrawals can be free but slower.

- Best for:

- Sellers and freelancers who already use PayPal and want faster access to their balance.

3) Square Instant Transfers

- What it is:

- Move your Square balance to a linked bank account 24/7/365.

- Key facts:

- Fee: 1.5% per instant transfers.

- New sellers may have a daily instant transfer limit (e.g., up to $500/day, growing up to $5,000/day).

- Square also offers next‑day payouts for free and instant access via the Square Cards.

- Best for:

- Small merchants, cafes, retail, and service businesses using Square’s POS.

4) Adyen Instant Card Payouts

- What it is:

- Pay out to Mastercard and Visa cards instantly via a single API call.

- Key facts:

- Funds typically available on the card within 30 minutes, often within ~2 minutes.

- Designed for use cases like:

- Seller payouts, marketplace disbursements, gaming winnings, refunds/claims.

- Part of Adyen’s broader “online payouts” and “on‑demand payouts” platform products.

- Best for:

- Larger platforms and marketplaces that need strong global coverage and card‑based instant payouts.

5) Real‑time bank / Pay‑by‑Bank gateways

- Revolut Gateway (Pay by Bank):

- Revolut has integrated Pay by Bank into its gateway, enabling instant bank‑to‑bank payments for merchants, with faster settlement and stronger security via Open Banking.

- Pay‑by‑Bank / open‑banking providers (Noda, etc.):

- Noda offers instant payout APIs sending money instantly via bank or card.

- Often marketed as “instant bank payments” or “pay‑by‑bank checkout + payout.”

- SEPA Instant–enabled bank APIs:

- Some banks and PSPs (e.g., Nordea’s Multi‑Payout Instant API) expose SEPA Instant payouts directly for automated bulk instant euro payments.

- Best for:

- Europe‑focused platforms that want account‑to‑account instant payouts without card rails.

- Reducing card fees and chargebacks while still providing instant settlement.

6) Payout‑API platforms and global payout providers

Payment gateway instant payout; These aren’t classic “gateways” for accepting payments, but they’re critical for instant payouts to your users:

- Wise Platform:

- Provides global mass payouts and multi‑currency accounts; 74% of transfers were instant as of late 2025.

- Good for low‑cost cross‑border payouts but not always “instant” in every corridor.

- Airwallex:

- Offers global business accounts, local payouts, and FX; often same‑day or faster depending on corridor and rail.

- Brite Payments:

- Focuses on instant bank‑to‑bank payments in Europe; claims payouts delivered in seconds over its proprietary network.

- Noda:

- Instant payout APIs via bank or card; emphasizes instant bank payments with open banking rails.

- Others:

- Dots, Trolley, Tipalti, Pinelabs, Aeropay, etc., specialize in payout automation and, in some cases, real‑time rails or same‑day capabilities.

- Best for:

- Marketplaces, gig platforms, and SaaS that need global payouts, FX, and increasingly instant/real‑time options.

7) Crypto/USDC instant payout gateways (niche)

- Some solutions (e.g., WHMCS “Instant Payment Gateway” modules) offer instant crypto/USDC payouts directly to your own wallet with finality and no chargebacks.

- Best for:

- High‑risk or crypto‑native businesses and users comfortable with volatility and wallet management.

5. What does instant payout typically cost?

Payment gateway instant payout; Cost structures vary by provider and rail. Common patterns:

- Card‑based instant payouts (to debit card):

- ~1–1.5% of the payout amount:

- Stripe: 1.5%, minimum 50¢ per Instant Payout.

- Square: 1.5% per Instant Transfers.

- PayPal: ~1.5% for an instant bank/card transfer.

- You also pay the standard card processing fee on the original payment (e.g., Stripe ~2.9% + 30¢ in the US).

- ~1–1.5% of the payout amount:

- Real‑time bank payout (account‑to‑account):

- Fee models can be:

- Percentage only (e.g., 0.5–1%),

- Fixed per transaction (e.g., a few cents per instant payment),

- Subscription + per‑transaction (some payout‑API platforms like Dots use this model).

- Some banks/PSPs charge for instant payments on top of scheme fees (e.g., SEPA Instant fees may apply at the bank level).

- Fee models can be:

- International instant payouts:

- Often include FX spreads (e.g., Wise’s mid‑market rate plus a small percentage; Wise reports average fees around 0.53% and 74% instant by late 2025).

- Cross‑border rails like UPI/PIX/SEPA Instant can still be fast but FX and corridor availability matter.

Rule of thumb:

- Card instant payouts = fast and easy, but relatively expensive at scale.

- Bank‑based instant payouts = can be cheaper, especially domestically, but depend on rail availability and provider integrations.

6. Geographic differences: where instant payouts work well

- United States:

- Real‑time rails: FedNow and RTP are now widely available for instant bank‑to‑bank payments.

- Many gateways still rely on card‑network instant payouts (Stripe, Square, Adyen) because they’re broadly supported.

- Europe (SEPA zone):

- SEPA Instant Credit Transfer: funds available within 10 seconds, 24/7.

- EU Instant Payments Regulation is driving all PSPs to support instant payments by 2025–2026.

- Gateways and PSPs like Brite, Revolut (Pay by Bank), and some local banks expose instant payouts via SEPA Instant.

- United Kingdom:

- Faster Payments is already near‑real‑time; Pay by Bank (open banking) is increasingly used for both checkout and payouts.

- India, Brazil, others:

- UPI and PIX are instant/24/7 and used heavily by local gateways and fintechs.

For a global platform, you’ll often combine multiple providers:

- Card instant payouts in the US/elsewhere.

- Bank instant payouts in SEPA/UK/India/Brazil.

- A payout‑API layer to orchestrate.

7. Implementation patterns for instant payouts

A) If you just want faster access to your own funds

- Step 1: Choose a gateway with instant payouts:

- Stripe, Square, PayPal, Adyen, or a local acquirer that supports instant payouts in your country.

- Step 2: Link an eligible payout destination:

- Business debit card that supports instant payouts, or

- Bank account in a supported country/rail.

- Step 3: Enable and configure:

- Turn on Instant Payouts/Instant Transfers in the dashboard or via API.

- Understand:

- Fees (e.g., 1.5%).

- Limits (daily/transaction caps).

- Cut‑off times (if any).

- Step 4: Decide when to trigger payouts:

- Automatically after every payment?

- At a threshold (e.g., balance > $500)?

- Manually on demand?

- Step 5: Monitor:

- Payout status, fees, and bank reconciliation.

B) If you’re building instant payouts for your users (platform/marketplace)

Payment gateway instant payout; Architecturally, you’ll typically:

- Underwrite and KYC your users

- Collect identity and banking details.

- Run KYC/AML checks (often via the PSP’s onboarding tools).

- Accept and split payments

- Use Connect/for‑Platforms products (Stripe Connect, Adyen for Platforms, etc.) so payments are split and each user has a sub‑balance.

- Choose payout rails per user/country

- Card: where fast access is critical and users accept ~1% fee.

- Bank (real‑time): where cheaper rails exist and users’ banks support SEPA Instant, Faster Payments, FedNow, UPI, PIX, etc.

- Call the payout API

- Example flows:

- Stripe Connect Instant Payouts for eligible users.

- Adyen Instant Card Payouts / On‑demand Payouts.

- Wise Platform / Airwallex / Brite / Noda for bank‑based instant or same‑day payouts.

- Handle statuses and errors

- Use webhooks to track:

- Payout created, in_transit, paid, failed.

- Implement retry logic and user notifications.

Payment gateway instant payout; Many platforms start with card‑based instant payouts (easier, more universal) and then add real‑time bank rails by region as they scale.

8. Pros and cons of instant payouts

Pros

- Better cash flow:

- You or your users get funds within minutes instead of days.

- Competitive advantage:

- Marketplaces and gig platforms can attract and retain sellers/workers by paying instantly.

- Improved UX:

- “Get paid now” buttons and instant withdrawals reduce frustration.

- Lower working capital needs:

- For gig workers and small sellers, instant access reduces the need for credit.

Cons / trade‑offs

- Higher fees:

- 1–1.5% per payout on top of normal processing fees can add ups.

- Limits and eligibility:

- Daily caps, country/rail restrictions, and account history requirements (e.g., new Stripe users aren’t immediately eligible).

- Fraud & risk:

- Instant payouts increase risk; you must:

- Reserve funds.

- Use risk scoring and holds.

- Handle disputes and clawbacks.

- Instant payouts increase risk; you must:

- Operational complexity:

- More payout options mean more reconciliation, support, and error handling.

9. Compliance, risk, and operational considerations

- Regulatory:

- Ensure you comply with local rules when sending payouts (e.g., AML, sanctions screening, licensing).

- In the EU, instant payouts via SEPA Instant will increasingly require payee verification under the IPR and Verification of Payee schemes.

- Fraud & chargebacks:

- With instant card payouts, chargebacks can still come days later.

- Best practices:

- Use rolling reserves or per‑user limits.

- Delay or partially hold payouts for higher‑risk users.

- Combine with strong identity verification.

- Bank coverage and rail availability:

- Not every bank supports FedNow, RTP, SEPA Instant, or card instant payouts.

- PSP eligibility can vary by country and account type.

- Reconciliation:

- Instant payouts can make reconciliation trickier because they occur outside standard batch windows.

- Use PSP reports and webhooks, and map them to your internal ledger.

10. How to choose the right instant payout solution

Payment gateway instant payout; Start from your use case and region:

- For simple, small‑business instant access to your own funds:

- Check Stripe Instant Payouts, Square Instant Transfers, or PayPal Instant Transfer depending on where you operate and what you already uses.

- For US‑centric marketplaces/gig platforms:

- Stripe Connect Instant Payouts (card + some bank rails).

- Adyen for Platforms with instant card payouts and on‑demand payoutsdocs.

- Payout‑API providers that integrate FedNow/RTP for bank‑instant payouts.

- For Europe/UK:

- SEPA Instant–enabled providers:

- Brite (instant bank payouts).

- Revolut Gateway with Pay by Bank.

- Direct bank integrations like Nordea’s Multi‑Payout Instant APInordea .

- Wise Platform for low‑cost cross‑border instant/same‑day payouts where availablewise .

- SEPA Instant–enabled providers:

- For global platforms:

- Combine a global gateway (Stripe/Adyen) for payments with a payout‑API provider for global disbursements:

- Wise Platform, Airwallex, Dots, Trolley, etc..

- Use a real‑time orchestration layer (e.g., Lightspark Grid) if you need unified API access across multiple instant railslightspark .

- Combine a global gateway (Stripe/Adyen) for payments with a payout‑API provider for global disbursements:

Key selection criteria:

- Geography & rail coverage:

- Which countries and payout rails (card, FedNow, RTP, SEPA Instant, UPI, PIX) must you support?

- Cost structure:

- Percentage vs. flat fees, FX spreads, minimums, and monthly platform fees.

- API & integration quality:

- Webhooks, idempotency, bulk payout support, error codes.

- Compliance tooling:

- KYC/onboarding, sanctions screening, reporting.

- Limits & scaling:

- Throughput limits, payout size caps, and SLAs.

11. Quick checklist to get started

- Decide your scope:

- Instant payouts to your own business only?

- Instant payouts to your users (sellers, workers, creators)?

- Pick your primary gateway/PSP:

- Stripe, Square, PayPal, Adyen, local acquirer, or marketplace‑oriented provider?

- Enable instant payouts:

- Confirm supported payout methods (card, bank) and countries.

- Understand pricing and limits.

- Link eligible bank accounts/debit cards.

- Configure policies:

- Auto vs. manual payouts.

- Minimum/maximum amounts and frequency.

- Risk settings (limits, holds, reserves).

- Integrate & test:

- Use test accounts and test card/bank numbers to simulate instant payouts.

- Implement webhooks and reconciliation.

- Monitor and iterate:

- Track payout success rates, fees, and user feedback.

- Expand to additional rails (e.g., real‑time bank transfers) as volume grows.

If you share:

- Your country/regions,

- Whether you need payouts just for yourself or for thousands of users,

- Your typical volume and average ticket size,

Payment gateway instant payout; I can narrow this down to a shortlist of 2–3 providers and a concrete integration pattern for 2026.

[…] on civil discourse, community, and a bygone era of American public life 🏞️📻 Also read, Payment gateway instant payout, Get paid […]