Features of Controlling Functions; Controlling is the last function of the management process which is performed after planning, organizing, staffing and directing. On the other hand, management control means the process to be adopted in order to complete the function of controlling.

Here are explain; What are the Features of Controlling Functions?

Following are the characteristics of controlling functions of management

- Controlling is an end function: A function which comes once the performances are made in-Conformities with plans.

- It is a pervasive function: which means it is performed by managers at all levels and in all type of concerns.

- Controlling is forward-looking: because effective control is not possible without past being controlled. Control always look to the future so that follow-up can make whenever to require.

- Controlling is a dynamic process: since controlling requires taking reviewal methods, changes have to be made wherever possible.

- It is related to planning: Planning and Controlling are two inseparable functions of management. Without planning, controlling is a meaningless exercise and without controlling, planning is useless. Planning presupposes controlling and controlling succeeds in planning.

Controlling has got two basic Process of Controlling:

- It facilitates coordination.

- It helps with planning.

Also, know about; What is Controlling?

Controlling consists of verifying whether everything occurs in conformities with the plans adopted, instructions issued and principles established. Control ensures that there is effective and efficient utilization of organizational resources so as to achieve the planned goals. Controlling measures the deviation of actual performance from the standard performance discovers the causes of such deviations and helps in taking corrective actions.

What are the Features of Controlling Functions? #Pixabay.Lets reading Definitions about Controlling; According to Brech,

“Controlling is a systematic exercise which is called as a process of checking actual performance against the standards or plans with a view to ensuring adequate progress and also recording such experience as is gained as a contribution to possible future needs.”

According to Donnell,

“Just as a navigator continually takes reading to ensure whether he is relative to a planned action, so should a business manager continually take reading to assure himself that his enterprise is on the right course.”

According to Henry Fayol,

“Control consists of verifying whether everything occurs in conformity with the plan adopted, the instructions issued, and the principles”.

Important Features of Controlling:

Features of controlling could describe in the following analytical manner:

- The unique feature of controlling, and.

- Other features of controlling.

Now, explain each;

Unique Feature of Controlling:

The unique feature of control is that it is the “central-tendency point” in the performance of managerial functions i.e. a point where all other managerial functions come together and unite with one another. This is so because, while contemplating corrective action, sometimes it might be necessary to modify plans or effect changes in the organizational setting. At some other times, changes in the staffing procedures and practices might be thought fit by management for remedial reasons.

While at some junctures, management might plan to effect changes in the directing techniques of leadership, supervision or motivation, to bring performance on the right track. That is to say, that the remedial action comprised in the controlling process might embrace one or more managerial functions. Hence, controlling is designated as the central tendency point, in management theory.

Other Features of Controlling:

Some important basic features of controlling could state as under;

- Controlling makes for a bridge between the standards of performance and their realistic attainment.

- Planning is the basis of controlling; in as much as, the standards of performance are laid down in plans.

- Controlling is a pervasive management exercise. All managers, at different levels in the management hierarchy, perform this function, in relation to the work done by subordinates under their charge-ship.

- As controlling is the last managerial function, it is true to assert that it gives a finishing or final touch to the managerial job, at a particular point of time.

- Controlling is based on information feedback i.e. on the reports on actual performance done by operators. In specific terms, it could say that information is the guide to controlling; as without information feedback made available to management, analysis of the causes of deviations and undertaking remedial action are not possible.

- Action is the soul of controlling. In fact, controlling would be a futile activity; if after analyzing deviations – suitable remedial action is not undertaking by management, to bring performance, in conformity with plan standards.

- Controlling is a continuous managerial exercise. It has to undertake on a regular and continuous basis, throughout the currency of the organizational operational life.

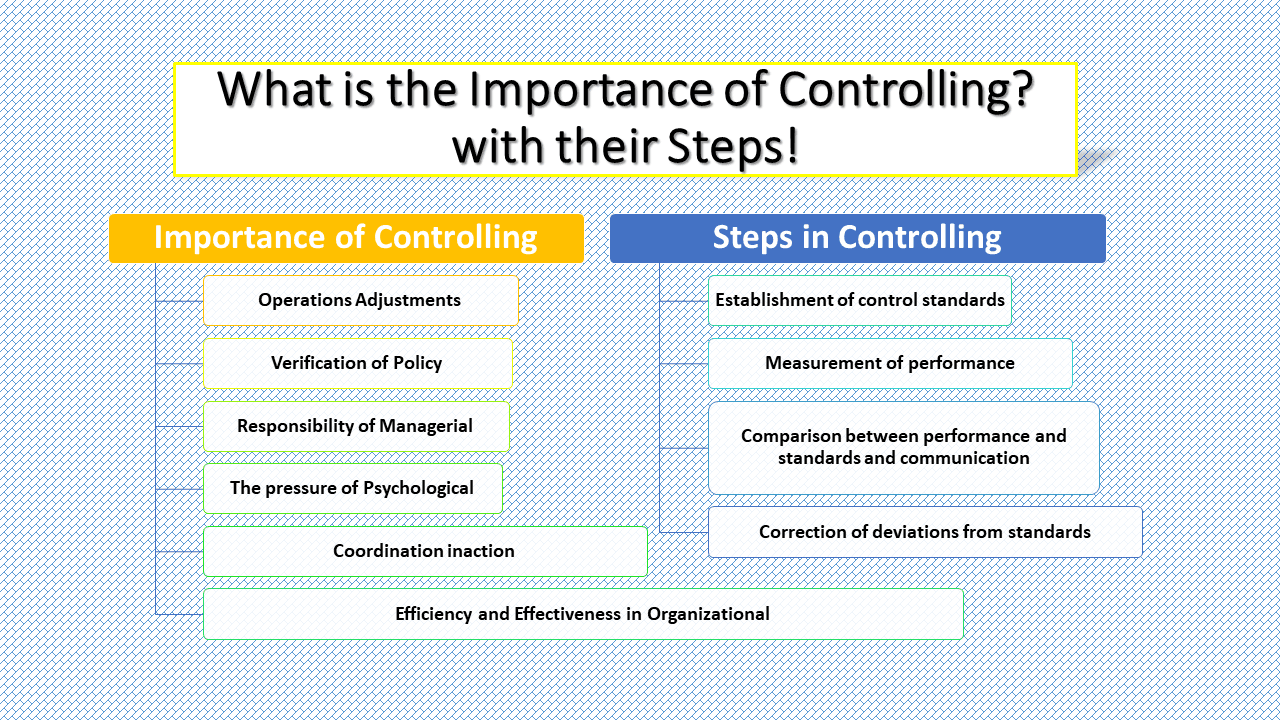

Significances of Controlling:

The significances of the controlling function in an organization are as follows:

- Accomplishing Organisational Goals: Controlling helps in comparing the actual performance with the predetermined standards, finding out deviation and taking corrective measures to ensure that the activities are performing according to plans. Thus, it helps in achieving organizational goals.

- Judging Accuracy of Standards: An efficient control system helps in judging the accuracy of standards. It further helps in reviewing & revising the standards according to the changes in the organization and the environment.

- Improving Employee Motivation: Employees know the standards against which their performance will be judged. Systematic evaluation of performance and consequent rewards in the form of increment, bonus, promotion, etc. motivate the employees to put in their best efforts.

Boundaries of Controlling:

The defects or boundaries of controlling are as following:

- Difficulty in Setting Quantitative Standards: It becomes very difficult to compare the actual performance with the predetermined standards if these standards are not expressing in quantitative terms. This is especially so in areas of job satisfaction, human behavior and employee morale.

- No Control on External Factors: An organization fails to have control of external factors like technological changes, competition, government policies, changes in the taste of consumers, etc.

- Resistance from Employees: Often employees resist the control systems since they consider them as curbs on their freedom. For example, surveillance through CCTV (closed-circuit television).

Leave a Reply