SR-22 isn’t actually insurance — it’s a certificate. How to Get SR-22 Insurance? Learn exactly what it is, which states require it, how much premiums increase, and how to find the cheapest SR-22 provider in 2026.

How to Get SR-22 Insurance in 2026: What It Is, How Much It Costs & Who Files It

Here’s the bottom line, then the details.

Bottom line (quick take)

- SR‑22 is not insurance. It’s a certificate your insurer files with the state to prove you have at least the minimum liability coverage required by law. Only an insurer can file it for you.

- Most states require SR‑22 after serious violations (DUI, driving without insurance, repeated offenses, etc.). How to Get SR-22 Insurance; A few states use their own forms instead (MA, MI, NJ, NY); Florida and Virginia use a stricter form called FR‑44 for DUIs (higher liability limits).

- The SR‑22 “filing fee” is usually small (often around $15–$25), but your underlying car insurance premium usually jumps because you’re now classified as high‑risk. WalletHub’s analysis finds SR‑22 “insurance” (a regular policy with an SR‑22 filing) averages about $1,204/year and can raise a driver’s premium up to about 103%; another WalletHub study suggests an average premium increase around 18% for drivers who need an SR‑22, but the actual hit depends heavily on your state, violation, and insurer.

- In California, for example, drivers with a DUI average about $180/month for state‑minimum SR‑22 coverage vs. $72/month for clean‑record drivers (roughly +150%).

- You don’t “buy an SR‑22” from a separate company. You buy an auto policy (or a non‑owner policy) from an insurer that offers SR‑22 filings and they file the form. The cheapest SR‑22 provider is usually a standard carrier that’s competitive for high‑risk drivers (often GEICO, AAA, and sometimes strong regional carriers like Wawanesa, Grange, Country, or Hastings in certain states).

- The key to finding the cheapest SR‑22 provider: comparison‑shop nationally (GEICO, Progressive, etc.) plus strong regional carriers, ask for every discount, consider higher deductibles, keep coverage continuous (a lapse can reset the clock), and check a non‑owner policy if you don’t own a car.

What SR‑22 actually is (and isn’t)

- It’s a certificate of financial responsibility. Your insurance company files the SR‑22 with the state DMV to certify that you carry the required liability coverage. The SR‑22 itself doesn’t provide coverage; your underlying auto policy does.

- People often say “SR‑22 insurance,” but that’s shorthand. It’s really:

- A regular car insurance policy, and

- An SR‑22 endorsement/certificate filing attached to it.

- Only an auto insurer can file an SR‑22 with the state. How to Get SR-22 Insurance; You cannot file it yourself.

Who needs an SR‑22?

How to Get SR-22 Insurance; Courts or state DMVs typically require an SR‑22 after serious violations such as:

- DUI / DWI

- Driving without insurance or without enough coverage

- At‑fault accident while uninsured

- Reckless driving

- Driving with a suspended/revoked license

- Multiple moving violations in a short period

- Hit‑and‑run or street racing

- Certain other serious offenses (e.g., some drug‑related driving offenses)

Virginia is a good concrete example: the DMV says SR‑22 certification is required for unsatisfied judgments, uninsured motor vehicle suspensions, falsifying insurance info, and certain license suspensions from serious convictions; FR‑44 is required for DUIs and some related offenses.

In practice, you usually find out you need an SR‑22 in one of two ways:

- A judge or court order tells you at a hearing.

- The state DMV/bureau sends you a letter saying you must file an SR‑22 to reinstate or keep your driving privileges.

Types of SR‑22 certificates (what you’ll choose)

How to Get SR-22 Insurance; Insurers generally offer three “flavors” of SR‑22 filings:

- Owner’s SR‑22: Covers vehicles you own (typical if you have a car registered in your name).

- Operator’s (non‑owner) SR‑22: Covers you as a driver, even though you don’t own a car. Requires a “non‑owner” liability policy.

- Owner‑Operator SR‑22: Covers you for any vehicle you drive, whether you own it or not.

What to pick:

- You own a car and drive it: Owner’s SR‑22.

- You don’t own a car but need to reinstate your license: Non‑owner SR‑22.

- You own a car but also often borrow/rent vehicles: Owner‑Operator SR‑22 if your state offers it.

Which states require SR‑22 (and for how long)

How to Get SR-22 Insurance; Most states use SR‑22, but the exact duration and the offense that triggers it vary a lot. A few states don’t use SR‑22 at all; Florida and Virginia have a stricter FR‑44 form for DUI cases. Here’s the high‑level picture as of 2026:

- States that do NOT use SR‑22 (they use their own systems):

- Massachusetts (uses FR‑1/FR‑19 forms)

- Michigan (no SR‑22 in its no‑fault system)

- New Jersey (uses its own DMV system)

- New York (uses an FS‑1 form and its own requirements)

- Florida and Virginia’s special rules (FR‑44 for DUI):

- For non‑DUI violations (e.g., driving without insurance) they use SR‑22 with usual minimum limits.

- For DUI they require FR‑44, which forces higher liability limits (often multiples of state minimums). Florida’s FR‑44 limits are much higher than its normal minimums, making premiums especially high.

- Typical SR‑22 durations in SR‑22 states (high‑level):

- Shortest: North Dakota — 1 year.

- On the long side: Nebraska and Tennessee can require 5 years for a DUI.

- A small group is 2 years: Iowa, Missouri, Texas.

- The majority of SR‑22 states are 3 years (e.g., AL, AZ, AR, CA, CO, CT, DE, FL SR‑22, GA, HI, ID, IL, IN, KY, LA, ME, MD, MN, MS, MT, NV, NH, NC, OH, OK, OR, PA, RI, SC, SD, UT, VT, WA, WV, WI, WY).

- Virginia and Florida generally require 3‑year filings as well, with FR‑44 for DUI; Tennessee is 3 years generally but can go up to 5 for DUI.

Important: these durations are per‑state summaries; always confirm with your state DMV or Department of Insurance because details can change and courts sometimes impose longer requirements.

If you move states with an active SR‑22

How to Get SR-22 Insurance; Your SR‑22 obligation generally “travels with you” based on the state that ordered it, not automatically the new state’s rules.

- Scenario 1: You have an SR‑22 in State A and move to State B.

- State A’s filing requirement usually still applies for its ordered period.

- If your insurer is licensed in both states, they can often keep filing with State A from your new address in State B.

- If coverage lapses during the move, many states reset the clock and you may have to start the filing period over.

- Scenario 2: You commit an offense in State A while you’re licensed in State B.

- State A may suspend your privilege to drive there and require an SR‑22/FR‑44 with their DMV.

- State B might still require its own financial responsibility filing for your license.

- You may need to satisfy both states’ requirements.

How to Get SR-22 Insurance; Two separate pieces of cost:

1) SR‑22 filing fee (usually small)

- A one‑time (or per‑term) fee for the insurer’s paperwork and electronic filing. This is often around $15–$25, but some states allow slightly higher amounts. Progressive, for example, says the filing fee is about $25, and WalletHub notes a typical $15–$25 range.

- Insurers often charge this each policy term (e.g., every 6 months) while the SR‑22 is required.

- SR‑22 itself isn’t insurance; you’re paying more because the violation that made you need an SR‑22 moves you into a high‑risk category, and many insurers price you higher.

- WalletHub’s nationwide analysis finds:

- SR‑22 “insurance” (a policy with an SR‑22 filing) averages around $1,204 per year, and an SR‑22 requirement can raise a driver’s premium by up to about 103%.

- Another WalletHub study on cheapest SR‑22 companies notes that, on average, an SR‑22 requirement raises premiums by up to roughly 18% (with variation by driver profile).

- California example (MoneyGeek, 2026):

- Clean‑record drivers: average about $72/month for state‑minimum coverage.

- Drivers with a DUI who need SR‑22: average about $180/month for state‑minimum coverage.

- That’s roughly a 150% increase in this California sample. GEICO shows entry‑level SR‑22 minimum coverage starting at about $108/month in CA, compared with that $72 clean‑record baseline.

How big your increase will be depends on:

- What you did (DUI vs. no insurance vs. other violation)

- Your state’s rules (especially FR‑44 in FL/VA vs. regular SR‑22 elsewhere)

- Your insurer’s appetite for high‑risk business

- Your age, location, vehicle, and other rating factors (in states that allow credit scoring, credit can affect the rate too; California bans credit‑based scoring for auto, so SR‑22 rates there reflect driving record more directly).

Who files the SR‑22 and how it works

How to Get SR-22 Insurance; You don’t file the SR‑22 yourself. Your insurer does. Here’s the flow:

Key points:

- Only auto insurers can file SR‑22 with the DMV.

- Most insurers will file electronically; some states encourage or require electronic filing for faster processing.

- If your current insurer won’t file SR‑22 (some carriers don’t), you must find one that does and buy a policy with them; they then file it.

- If the policy lapses or cancels during the SR‑22 period, the insurer typically notifies the state and you can face new suspensions and/or a reset of the filing period.

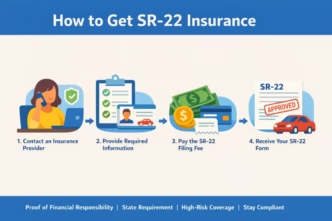

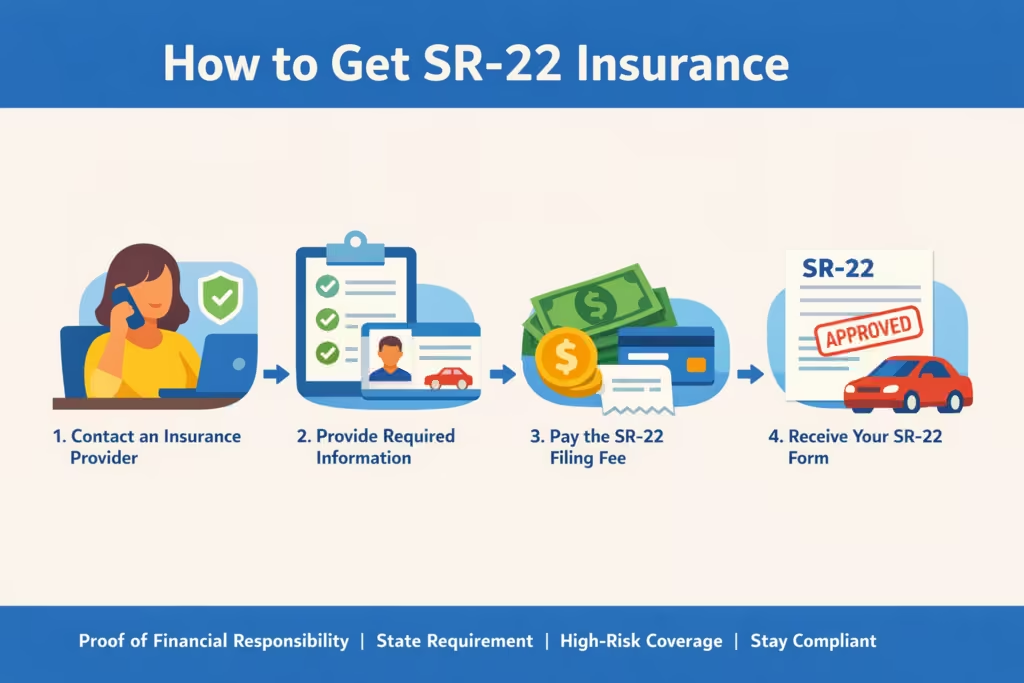

How to get SR‑22 (step‑by‑step in 2026)

Confirm you actually need it and for how long

- Check your court order or any letter from your state DMV/bureau of motor vehicles.

- Note:

- Required filing type: SR‑22 vs. FR‑44 (in FL/VA) vs. your state’s own form (e.g., MA/MI/NJ/NY).

- The filing period (e.g., 3 years) and start date.

- Required liability limits (especially higher limits for FR‑44).

Decide what type of certificate you need (owner, operator, owner‑operator)

- Do you own a car? Owner’s SR‑22.

- Don’t own a car? Non‑owner SR‑22 (operator).

- Own a car and often drive others’ cars too? Ask whether your state allows an owner‑operator filing and whether it’s right for you.

Make sure your liability limits meet the state (and FR‑44 if applicable)

- Minimum required liability varies by state.

- For FR‑44 (FL/VA DUIs), the law sets higher limits than the normal minimums; Virginia’s DMV explicitly notes FR‑44 limits are double SR‑22 limits in its code, and Florida’s FR‑44 limits are even higher. That directly increases premiums.

Contact your current insurer (or find one that does SR‑22)

- Ask your current company:

- Do you file SR‑22s in my state?

- What is the filing fee?

- How will I be charged (one‑time vs. per term)?

- If they say no, you’ll need to shop for a new insurer that does SR‑22 filings; many large and midsize carriers do, but some smaller ones don’t.

Buy or adjust the policy and have the insurer file

- If you already have a policy: they’ll add an SR‑22 endorsement and file it with the state.

- If not: buy at least the state minimum liability (or the higher FR‑44 limits if required) on a new policy and have them file.

- If you don’t own a car: buy a non‑owner liability policy and have them file the operator SR‑22.

Confirm the filing was accepted

- Ask your insurer for confirmation that the SR‑22 (or FR‑44) was filed and the effective date.

- Verify with your state DMV online or by phone if possible (some states show financial responsibility filings online).

Keep coverage continuous — no lapses

- A lapse during the filing period typically triggers:

- Another suspension or fine, and

- Often a reset of the filing requirement clock.

- Set up autopay and paperless so a missed payment doesn’t accidentally cancel you.

When the mandated period ends, remove the SR‑22

- SR‑22 filings usually don’t “fall off” automatically; you or your insurer must act.

- Ask your insurer in writing to remove the SR‑22/FR‑44 once your state’s required period is over, and confirm with the DMV that your status is clear.

How to Get SR-22 Insurance; You don’t just pay the SR‑22 filing fee. The main extra cost is that you’re now in a higher‑risk rating tier.

- National figures (WalletHub):

- SR‑22 “insurance” averages about $1,204/year nationally; the requirement can increase a driver’s premium by up to about 103% in some cases.

- Another WalletHub study focused on cheapest SR‑22 insurers finds the SR‑22 requirement raises premiums by up to about 18% on average, but this varies by state and violation.

- State‑specific example (California, 2026):

- Clean‑record drivers: ~$72/month for state minimum coverage.

- Drivers with a DUI needing SR‑22: ~$180/month for state minimum coverage — about a 150% jump.

- FR‑44 impact (Florida/Virginia):

- Because FR‑44 requires liability limits several times higher than normal minimums, premiums during an FR‑44 period are often much higher than for a standard SR‑22. How to Get SR-22 Insurance; One analysis notes Florida FR‑44 drivers can pay thousands more per year while the filing is active.

Why the jump?

- Insurers rate using the probability of future claims. Offenses like DUI, driving without insurance, and repeated violations are strong predictors of higher risk.

- SR‑22 flags you to the insurer as a recent serious violation; they adjust the rate accordingly.

- Each carrier has its own appetite for high‑risk drivers; that’s why premiums for the same SR‑22 situation can differ widely from one insurer to another.

How to find the cheapest SR‑22 provider in 2026

How to Get SR-22 Insurance; Because the underlying policy is just auto insurance with a filing, “cheapest SR‑22 provider” = insurer that:

- Files SR‑22s (or FR‑44) in your state, and

- Offers the lowest overall premium for your situation, after discounts and rating factors.

Based on 2026 analyses, here’s who tends to be competitive and how to shop:

Start with insurers known for competitive SR‑22 rates

WalletHub’s 2026 study of 26 major insurers finds GEICO and AAA tend to be the cheapest nationally for SR‑22 drivers, followed by carriers like Wawanesa, Grange, USAA, Progressive, etc.

- In California, MoneyGeek finds GEICO leads with minimum SR‑22 coverage starting at about $108/month, ahead of Progressive and others; the cheapest insurers for SR‑22 in CA aren’t always the same as for clean‑record drivers, so it really pays to compare.

- Regionals matter: WalletHub notes that regional carriers like Wawanesa (CA/OR), Country Financial, Grange, and Hastings Mutual often have some of the cheapest SR‑22 rates in their particular states.

Get quotes from multiple insurers — both national and strong regionals

- National names to consider (where they offer SR‑22 filings in your state): GEICO, AAA, Progressive, USAA (if military‑eligible), Allstate, Travelers, etc.

- Strong regional carriers to check (depending where you live): Wawanesa (CA, OR), Grange (about 13 states), Country, Hastings, and other companies with good high‑risk ratings in specific states.

- Use comparison sites that let you indicate you need an SR‑22 (or ask an independent broker who works with multiple high‑risk carriers).

Ask for every discount

Even with a violation, many discounts still apply. How to Get SR-22 Insurance; WalletHub notes carriers like GEICO and AAA are competitive not only on base rate but because they offer many discounts that can reduce your SR‑22 policy price.

Common discounts to ask about:

- Good driver (sometimes you still qualify if your current record is improving)

- Bundling (home + auto, renters + auto)

- Pay in full (or 6‑month payments)

- Paperless/autopay

- Good student (if applicable)

- Occupation/affinity or professional group discounts

- Low‑mileage or usage‑based programs if you don’t drive much

Adjust coverage smartly (but keep at least required limits)

- With FR‑44, you must maintain the higher statutory limits, so you can’t lower those. But you can:

- Raise collision/comprehensive deductibles if you have older cars to reduce premium.

- Drop collision/comprehensive on very low‑value vehicles (if the car is paid off and you can absorb the loss).

- With standard SR‑22, choose at least state minimums; carrying more liability than minimum is usually safer, but be aware that higher limits = higher premiums.

If you don’t own a car, look into a non‑owner SR‑22 policy

- A non‑owner liability policy with an SR‑22 filing satisfies the requirement when you don’t have a car.

- Progressive, GEICO, and some others offer non‑owner policies with SR‑22 filings; WalletHub notes GEICO offers non‑owner policies, which can be helpful if you don’t own a vehicle.

Avoid coverage lapses at all costs

- A lapse during the filing period often:

- Resets the clock (you may start the filing period over), and

- Leads to additional suspensions/fees.

- Practical safeguards:

- Enroll in autopay for at least the minimum.

- Turn on paperless and email/text alerts.

- If you must switch insurers, make sure the new policy is effective before the old one cancels, and that the SR‑22 is transferred without interruption.

Consider working with an independent agent or broker who specializes in high‑risk

- Brokers who work with many “non‑standard” carriers can save time because they already know:

- Which insurers in your state actually file SR‑22s.

- Which are lenient with your specific violation (e.g., DUI vs. no insurance).

- What discounts to stack for high‑risk drivers.

After the required period, confirm removal and shop again

- Ask your insurer (in writing) to remove the SR‑22/FR‑44 once the state‑mandated period is over.

- Check your DMV record to confirm the filing is no longer active.

- Then shop again: insurers treat you differently once the SR‑22 obligation ends. How to Get SR-22 Insurance; You may see much better rates from the same company or others after the filing drops off.

Quick SR‑22 checklist for 2026

- Verify with your state DMV: Do I need SR‑22 (or FR‑44 or another form), for how long, and what liability limits?

- Identify what certificate type you need: Owner, operator (non‑owner), or owner‑operator.

- Contact your current insurer: Do you file SR‑22s/FR‑44 in my state? What’s the filing fee?

- If they don’t file SR‑22: Get quotes from at least 3–5 insurers that do file it, including regionals known for cheaper SR‑22 rates (e.g., GEICO, AAA, and regional carriers like Wawanesa/Grange/Country where available).

- Make sure liability limits meet at least state minimums (or FR‑44 higher limits if applicable).

- Buy or adjust the policy and have the insurer file the SR‑22/FR‑44; get confirmation and verify with the DMV.

- Set up autopay and alerts so there’s no lapse during the filing period.

- Once the filing period ends, ask the insurer to remove the SR‑22/FR‑44 and re‑shop for better rates.

Leave a Reply