Startup Legal Structure LLC vs C-Corp; Choosing the wrong legal structure can block you from raising venture capital. Compare LLC and C-Corp tax treatment, investor compatibility, equity issuance, and Delaware incorporation for 2026.

Startup Legal Structure LLC vs C-Corp in 2026: Which Legal Structure Is Right for Raising VC?

Short answer (for 2026)

- If you’re building a high‑growth startup and plan to raise VC (or aim for an IPO/acquisition), the right choice in 2026 is overwhelmingly a Delaware C‑Corporation. Most institutional investors and VCs expect and often require it; data show around 93% of VC‑backed startups are Delaware C‑Corps.

- If you’re bootstrapping, consulting, or building a “lifestyle” business with no real VC plans, an LLC is usually simpler and more tax‑efficient in the early years.

Startup Legal Structure LLC vs C-Corp; Below is a decision framework and key trade‑offs tailored to 2026 rules and practice.

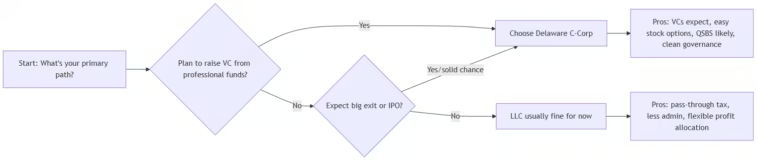

High‑level decision flow (LLC vs C‑Corp for VC path)

Why VCs strongly prefer C‑Corps (especially Delaware)

- Investor structure and tax issues with pass‑through entities:

- LLCs are pass‑through and issue Schedule K‑1s to members, which can create UBTI (unrelated business taxable income) problems for tax‑exempt LPs (pensions, endowments). Many VCs simply won’t invest through an LLC.

- Preferred stock and standardized deal terms:

- C‑Corps can issue multiple classes of stock (common, Series Seed/A/B preferred), which makes structuring liquidation preferences, board rights, and other investor protections straightforward. That’s a big reason C‑Corps are considered the “best option for raising venture capital.”

- LLC “membership interests” can be drafted to mimic preferred stock, but the documents are less standard, more expensive, and unfamiliar to many investors.

- Governance and board expectations:

- VCs expect a board of directors, officers, and standardized corporate governance—features baked into corporate law.

- Delaware law is the default investors rely on; the Court of Chancery and DGCL give predictability and a deep body of precedent.

- Compatibility with public markets and exits:

- C‑Corps can go public and are the standard structure for IPOs and many acquisitions. LLCs are rarely the IPO vehicle and make M&A more cumbersome.

- Market reality (2026):

- One 2026 analysis puts the share of VC‑backed startups that are Delaware C‑Corps at about 93%. That’s the de facto standard.

Startup Legal Structure LLC vs C-Corp; If you’re on a VC path, you’ll be swimming upstream the entire time as an LLC. Investors will either ask you to convert or pass.

Startup Legal Structure LLC vs C-Corp; Core differences at a glance (2026)

| Aspect | LLC | C‑Corp (typically Delaware) |

|---|---|---|

| Taxation | Pass‑through: income/loss flows to members’ 1040s; no entity‑level federal tax (by default) | Double taxation: 21% federal corporate tax on profits, then shareholders pay tax again on dividends/capital gains. Most startups reinvest profits, so double tax often isn’t material early on. |

| Investor friendliness | Many VCs won’t invest; tax and structural friction for institutional LPs; standard preferred‑stock deals don’t fit cleanly | Standard for VCs; can issue preferred stock and option plans; documents and governance are familiar. |

| Equity comp for employees | You grant “profits interests” or “membership interests”—less familiar and often more complex for employees/tax | Stock options and RSUs are straightforward; ISOs/NSOs are well understood; employees expect them. |

| QSBS (Sec. 1202) | Not QSBS stock; converting later can increase basis, but pre‑conversion appreciation doesn’t get the benefit and timing/limits get tricky | C‑Corp stock is QSBS‑eligible if requirements are met; 2025 law expanded exclusions to 50%/75%/100% for holdings of 3/4/5+ years. |

| Governance & formalities | Lighter: fewer formal meeting/minute requirements; flexible management | More formalities: board/ shareholder meetings, bylaws, minutes, stock ledger; investors like the clarity. |

| State choice flexibility | Most states are fine; some later investors may still want Delaware conversion anyway | Delaware is the default for VC deals and the standard investors expect. |

2026 tax landscape you should know

- Federal corporate rate: flat 21% for C‑Corps in 2026.

- QSBS (Sec. 1202) got a makeover:

- For QSBS issued after July 4, 2025, individual shareholders can exclude 50% of gains if held ≥3 years, 75% if held ≥4 years, and 100% if held >5 years—up to a cap (the greater of $15M or 10x basis, with the $15M inflation‑indexed from 2027).

- Only C‑Corp stock can be QSBS; LLC interests do not qualify.

- Starting as an LLC and later converting can increase your basis (and thus the 10x limit), but any built‑in gains before conversion are not eligible for QSBS exclusion, and the holding period only starts at conversion.

In practice:

- C‑Corp: Cleanest path to QSBS if you meet the asset and active‑business tests. This can be a huge exit‑tax benefit for founders and early employees.

- LLC‑then‑convert: Can sometimes juice your QSBS 10x basis if you convert when value is high, but it’s risky, adds legal/tax cost, and the holding‑period clock restarts at conversion. Startup Legal Structure LLC vs C-Corp; This is nuanced—don’t do it without professional advice.

How each choice impacts VC fundraising

Delaware C‑Corp

- What investors like:

- Familiar structure: they know exactly how preferred stock, liquidation preferences, protective provisions, and voting work.

- Clean tax profile: no K‑1 UBTI issues for tax‑exempt LPs.

- Standardized paperwork: NVCA‑style documents and financing customs are built around corporations.

- Easy option plans: you can set up a 409A equity incentive plan and issue ISOs/NSOs efficiently.

- Practical 2026 reality:

- Term sheets, lead investors, and crowdfunded equity rounds (e.g., Wefunder/SeedInvest) assume a C‑Corp.

- Many angels and accelerators also strongly prefer or require Delaware C‑Corp.

LLC

- Where it hurts in a VC process:

- Many VCs will ask you to convert to a C‑Corp before they sign term sheets.

- Deal lawyers need to craft “LLC preferred interests” or restructure via a holding corp, which adds time and legal fees.

- International investors or public‑company acquirers often dislike acquiring LLCs because of tax and governance frictions.

How each choice affects employees and equity comp

C‑Corp

- Stock options and RSUs are standard:

- ISOs and NSOs are well‑understood vehicles; employees and hires are used to getting option grants in a corporation.

- 409A equity plans are routine and can be approved with board/stockholder actions.

- Tax treatment is clear:

- ISOs can offer tax‑free growth until exercise if holding rules are met; NSOs are simpler but taxed differently.

- Recruiting advantage:

- Prospective employees in high‑growth startups expect stock options tied to a corporate structure; an LLC’s “profits interests” may confuse or worry them.

LLC

- Equity is usually “membership interests” or “profits interests”:

- Can be structured to resemble options, but they’re less standard; tax treatment for employees is more complex (often phantom equity or profits‑interest plans).

- High‑growth hiring:

- You can still grant equity, but you may need to layer in a C‑Corp holding company or convert later before offering traditional option packages.

Costs, admin, and practical pain

- LLC:

- Formation and annual state fees are generally low.

- Few formalities: no mandatory board/annual meetings in many states (though you should still keep decent records).

- Lighter administrative burden is great when you’re experimenting and pre‑revenue.

- C‑Corp:

- More formalities: board/ shareholder meetings, bylaws, consents, stock ledger upkeep.

- You’ll likely work with startup counsel and a bookkeeper/CPA to manage filings, cap table, and tax compliance (franchise tax, Delaware annual report, 1120, etc.).

- The extra work is basically the price of admission to serious VC financing.

When an LLC makes sense in 2026

- Good candidates for LLC:

- Bootstrapped or solo‑founder projects.

- Consulting, agencies, or content businesses where you’re not seeking institutional capital.

- Real estate or heavily pass‑through‑oriented businesses.

- Early testing of an idea where you might shut it down or pivot.

- Reasons to choose LLC:

- Simplicity and low overhead early on.

- Single‑level tax (pass‑through) can be advantageous while you’re paying ordinary income rates on modest profits.

Startup Legal Structure LLC vs C-Corp; Even then, be pragmatic: if it becomes clear within the first 12–18 months that this is a VC‑scale business, don’t delay converting to a Delaware C‑Corp.

When a Delaware C‑Corp is the clear winner

- Strong signals you should choose C‑Corp from day one:

- You plan to raise professional seed/Series A rounds within the next 12–24 months.

- You’re building in a sector where VC is the main growth capital (deep tech, biotech, infra, AI, etc.).

- You expect to hire a lot of employees and use equity as a major recruiting tool.

- An IPO or high‑value acquisition is part of the long‑term plan.

- Why it’s “right” for that path:

- Investors expect and often require it; not being a C‑Corp slows deals.

- It’s the structure that supports QSBS, clean option plans, and easy later‑stage financing.

Converting from LLC to C‑Corp: if you started “wrong”

- It’s possible, but it costs:

- Legal fees commonly run a few thousand dollars and take a few weeks (statutory conversion or merger/asset transfer).

- You’ll likely face tax analysis around asset transfers and valuations.

- QSBS interaction with LLC → C‑Corp:

- If you convert when value is already high, your basis for QSBS may be stepped up to FMV at conversion, which can increase the 10x basis limit (potentially allowing more tax‑free gain). But:

- Built‑in gains before conversion are not QSBS‑eligible.

- The QSBS holding period only starts at conversion.

- The entire business FMV at conversion must stay under ~$75M (indexed) to qualify.

- This strategy can be powerful but is complex; Orrick explicitly flags the risks and advises close work with tax advisors.

- If you convert when value is already high, your basis for QSBS may be stepped up to FMV at conversion, which can increase the 10x basis limit (potentially allowing more tax‑free gain). But:

- Practical tip:

- If you’re currently an LLC and even moderately serious about VC, at least get a professional assessment now. Startup Legal Structure LLC vs C-Corp; A well‑timed conversion can be cheaper and cleaner than a forced conversion right before a financing.

Quick checklist (2026)

Startup Legal Structure LLC vs C-Corp; You’re likely better off as an LLC if:

- You do not intend to raise from institutional VCs.

- You expect modest growth, profitability in the near term, or it’s a lifestyle business.

- You value minimal administrative overhead and simple taxation while you experiment.

You’re likely better off as a Delaware C‑Corp if:

- You plan to seek VC funding within the next ~18 months.

- You want to hire employees and grant stock options/RSUs as a standard part of comp.

- An IPO or strategic acquisition is a realistic long‑term goal.

- You care about preserving QSBS eligibility on clean, straightforward terms.

Practical “2026 play” most founders actually follow

- Stage 0–6 months (uncertain idea, no VC yet):

- Some founders still use an LLC for maximum flexibility.

- Others jump straight to Delaware C‑Corp because they already know they want a VC path.

- Stage 6–24 months (product/traction and preparing for a serious seed):

- If still an LLC, they proactively convert to Delaware C‑Corp before finalizing investors.

- They set up a 409A plan and clean cap table.

- Series A+:

- Company is already a Delaware C‑Corp; focus is on preferred‑stock terms, board composition, and QSBS planning.

Bottom line for 2026

- If you’re building a venture‑backable, high‑growth startup, you’re choosing not “if” you’ll be a C‑Corp, but “when.” Starting as a Delaware C‑Corp aligns you with what ~93% of VC‑backed startups do and what investors expect.

- If you’re not on that path, LLC’s flexibility and pass‑through taxation can be exactly what you need, with a possible conversion later if plans change.

Startup Legal Structure LLC vs C-Corp; None of this is personal tax or legal advice. Entity choice, conversion, and QSBS planning interact with your specific facts, state law, and tax status—get a startup‑savvy lawyer and a CPA to run your scenario before filing.

Leave a Reply